How to Open an International Merchant Account and Payment Gateway

Accepting payments from international customers isn’t always straightforward. Different currencies, payment methods, fraud risks, and banking rules can make cross-border payments complicated.

Without the right payment infrastructure in place, businesses may struggle with declined transactions, slow settlements, or limited payment options for customers abroad. That’s why you need a trusted international merchant account and payment gateway provider.

Let’s see how international merchant accounts work, who the best providers are, and how to set everything up — from getting the right documents to configuring the payment gateway.

QUICK TAKEAWAYS

- International merchant accounts allow businesses to accept payments from customers in multiple countries and currencies.

- The right payment setup can reduce currency conversion costs and improve global checkout conversion rates.

- High-risk merchants often need specialized international or offshore merchant accounts to process payments reliably.

- Opening an international merchant account typically requires business verification, various documentation, and website compliance checks.

- SecureGlobalPay offers an international merchant account and gateway for high-risk merchants.

The purpose of an international merchant account

An international merchant account is a type of bank account that allows businesses to accept and process payments from customers in multiple countries and currencies. Together with a payment gateway and payment processor, it helps securely authorize, process, and settle online payments from global customers.

There are multiple reasons to open an international merchant account:

- Accept payments from global customers: An international merchant account allows businesses to process payments from customers located in different countries, making it possible to sell products and services worldwide.

- Reduce payment friction: Customers are more likely to complete purchases when they can pay using their preferred currency and payment method.

- Reduce currency conversion costs: International merchant accounts often support multi-currency processing and settlement. This allows businesses to accept payments in different currencies and convert funds at more favorable exchange rates compared to standard domestic payment setups.

- Expand market reach: With the ability to accept international payments, businesses can enter new markets and grow revenue beyond their domestic customer base.

The main difference between a domestic and an international merchant account is the scope of payment processing. A domestic merchant account is typically designed to process transactions within a single country and currency, while an international merchant account allows businesses to accept payments from multiple countries, currencies, and sometimes a wider range of payment methods.

International merchant accounts are commonly used by e-commerce businesses, SaaS companies, subscription-based services, digital product sellers, travel companies, and online platforms that serve customers across multiple regions.

Furthermore, high-risk business industries — such as online gaming, forex trading, adult services, or nutraceuticals — often require international high-risk merchant accounts because many traditional banks are unwilling to work with them.

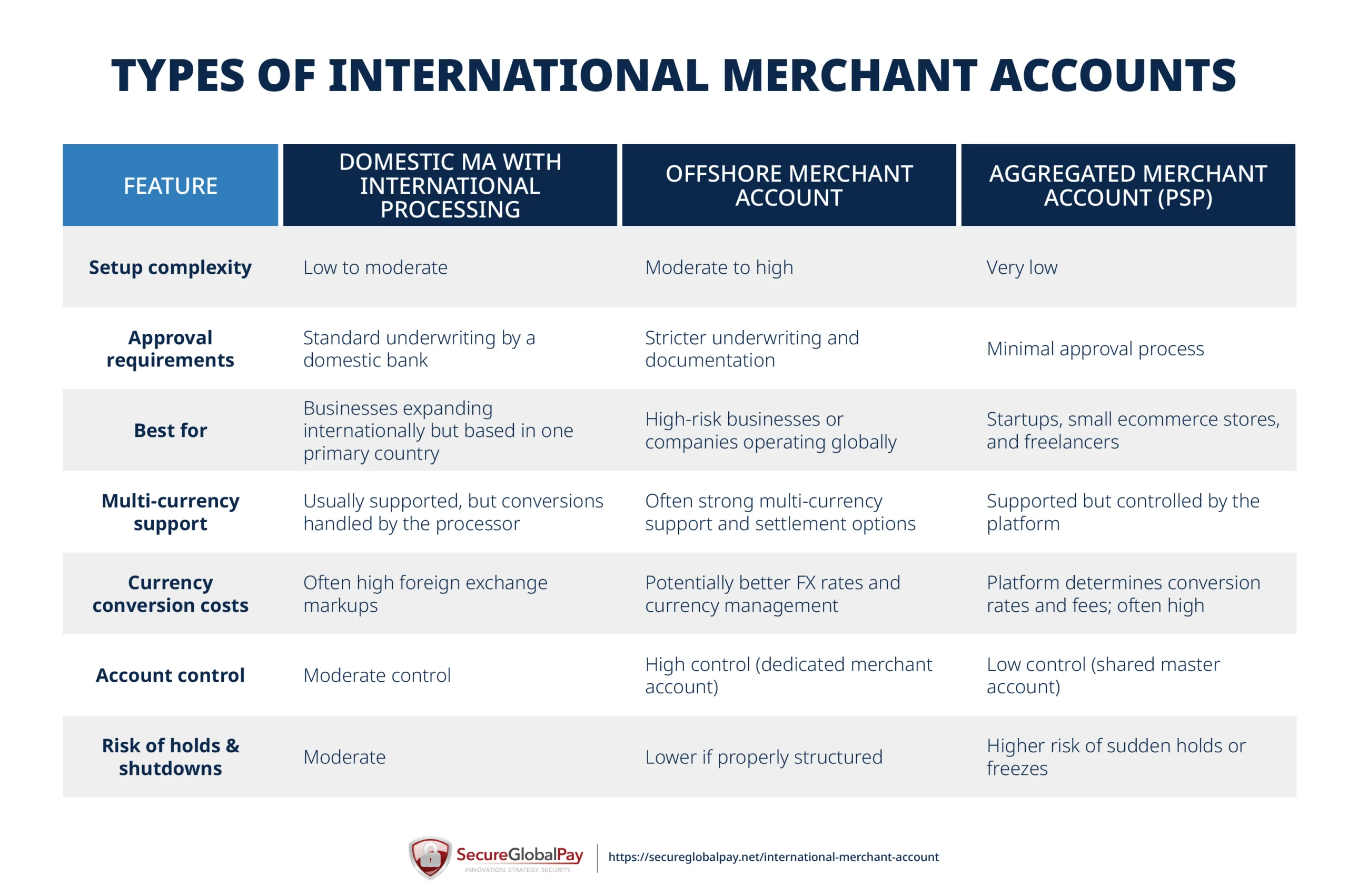

Types of international merchant accounts

Not all international merchant accounts are structured the same way. Depending on the business model, risk profile, and where a company operates, merchants may choose between several types of international payment setups.

The most common types include:

- Domestic merchant account with international processing: Some payment providers allow businesses to keep a domestic merchant account while still accepting international payments. This option is typically easier to set up but comes with higher cross-border and currency conversion fees.

- Offshore merchant accounts: Offshore merchant accounts are opened through acquiring banks located outside the merchant’s home country. These accounts are commonly used by businesses operating internationally or by companies in industries considered higher risk.

- Payment service providers (PSPs): Merchants can accept international transactions through platforms like Stripe, PayPal, or Square. This is the simplest setup to start with.

However, you have less control over payment processing, and constantly live in fear of sudden account holds or freezes.

PSPs are convenient for startups and small businesses. High-ticket, high-volume, and hard-to-place merchants use a dedicated high-risk international merchant account as it provides greater control, stability, and flexibility in payment processing.

The requirements for opening international high-risk merchant accounts

Opening an international merchant account, especially as a high-risk business, involves a comprehensive underwriting process.

Below are the most common requirements that payment providers and acquiring banks look at:

- Documentation requirements: Merchants must provide several documents to verify the legitimacy of the business and its owners. Common documents include business registration certificates, identification for company directors or owners, proof of address, bank statements, and sometimes financial statements or processing history from previous payment providers.

- Website compliance: The website, particularly for e-commerce businesses, must meet certain compliance standards before approval. This typically includes clear product descriptions, visible pricing, defined refund and return policies, simple terms and conditions, and secure checkout functionality.

- Industry-specific requirements for high-risk merchants: For example, firearms merchants need a valid Federal Firearms License (FFL), online gambling businesses may need a recognized gaming license, and CBD or nutraceutical sellers may need product compliance documentation, lab reports, or regulatory approvals. This ensures the business is legally allowed to sell its products and operate in the markets it serves.

Steps for opening an international or offshore merchant account

To open an international or offshore merchant account, you’ll often go through the following steps:

- Choosing a payment processor: Start by researching providers that support international payments and your specific business model. Look for factors such as supported countries, multi-currency support, payment methods, processing fees, fraud protection tools, and experience working with your industry.

- Preparing documentation: This usually includes company registration documents, identification for business owners, proof of address, bank statements, processing history (if available), and any industry-specific licenses or compliance documents.

- Submitting the merchant application: These days, many providers offer an online application. This form typically asks for details about your business model, expected transaction volume, product types, target markets, and specific documentation.

- Getting approved and signing the agreement: After submission, the payment provider’s underwriting team will review the application and assess the risk profile of the business. If approved, you will receive a processing agreement that outlines fees, reserve requirements, settlement terms, and other conditions.

- Integrating the payment gateway: Once the merchant account is activated, the payment gateway must be integrated into the business website, checkout, or e-commerce platform.

- Testing payment processing: Before going live, we recommend running a few test transactions to verify that payments are processed correctly, currencies are handled properly, and settlement flows into the merchant account as expected.

- Going live: After testing is successful, the payment system can be fully activated on the website. You are ready to accept payments from international customers.

Ideally, you will work with a provider like SecureGlobalPay that offers experienced support managers who can resolve any issues during the approval and setup process.

QUICK AND EASY ONLINE APPLICATION

We specialize in getting high-risk merchants approved and processing!

Top international merchant account providers

When choosing an international payment provider, focus on: supported countries, multi-currency support, currency conversion fees, accepted payment methods, gateway integration options, settlement times, and built-in fraud protection tools.

In other words, the right provider should support your target markets while offering reliable payment processing and reasonable fees.

Popular options for small businesses in low-risk industries include:

- Wise Business is known for competitive currency conversion rates and international transfers.

- Stripe and Square offer powerful, developer-friendly payment integrations for online businesses.

- PayPal Open remains a strong choice for e-commerce merchants who want a quick and familiar payment option for customers.

Popular options for high-risk businesses include:

- SecureGlobalPay: A merchant service provider that offers domestic and offshore merchant accounts specifically designed for high-risk industries. You get an integrated payment gateway, transparent pricing, and dedicated customer support.

- EMerchantBroker (EMB): A well-known provider that specializes in payment processing for high-risk industries and offers international merchant account solutions with dedicated support for regulated or higher-risk sectors.

- Durango Merchant Services: Offers offshore merchant accounts and payment processing for high-risk industries such as CBD, travel, and online subscriptions.

- Corepay: A payment processor that specializes in merchant accounts for high-risk and regulated industries. Corepay supports international payment processing, multiple currencies, and custom payment solutions for businesses operating across different markets.

Free Template for Comparing Merchant Service Providers

Our Google Sheet template arms you with 13 critical questions you should ask each provider to catch red flags and cut through the sales talk — with SecureGlobalPay’s answers already filled in for comparison.

Costs involved in international payment processing

The cost of processing international payments varies depending on the payment provider, the merchant’s risk profile, and the countries where payments are processed.

Common costs associated with international payment processing include:

- Setup fees: Some merchant account providers charge an initial setup fee (up to $500) to establish the merchant account and configure the payment gateway. This fee may also cover onboarding, underwriting, and technical integration support.

- Transaction fees: This is the percentage charged on each processed transaction. For international payments, merchants usually pay around 2.9% to 4.5% + $0.30 per transaction. High-risk businesses may see rates between 3.9% and 6.5%, depending on the industry.

- Cross-border fees: When a customer’s card is issued in a different country from the merchant account, card networks may apply additional cross-border charges. These fees are typically 1% to 2% per transaction on top of the standard processing fee.

- Currency conversion fees: If a transaction is processed in one currency but settled in another, the payment provider may apply a conversion fee or FX markup. This usually ranges from 1% to 3% above the base exchange rate.

- Chargeback fees: When a customer disputes a transaction, payment processors charge a fee to handle the dispute process. These fees generally range from $20 to $100 per chargeback, depending on the payment provider and the merchant’s risk level.

- Monthly account fees: Some providers charge a recurring fee to maintain the merchant account, use the payment gateway, and access fraud monitoring tools. These fees typically range from $35 to $75 per month.

While these fees can add up, the right provider can offer a secure, reliable, and scalable international payment infrastructure that supports global business growth.

For an in-depth look, check out our guide on high-risk merchant account fees and rates.

Get a high-risk international merchant account and payment gateway with SecureGlobalPay

SecureGlobalPay is an all-in-one merchant services provider. We offer both domestic and international merchant accounts, along with integrated payment gateway solutions designed specifically for high-risk merchants.

By working with multiple acquiring banks and payment networks, SecureGlobalPay can help businesses in regulated or higher-risk industries access reliable payment processing across the globe.

Some of the benefits of working with SecureGlobalPay include:

- International and offshore merchant accounts for businesses operating in global markets.

- A robust, integrated payment gateway for secure online transactions through your website (checkout), app, e-commerce platform, or store.

- Multi-currency payment processing for accepting payments from customers worldwide.

- Multi-MID setup with automatic routing for high-volume merchants.

- Fraud prevention and chargeback management tools to help reduce risk and costs.

- Expert support: Each client gets an industry veteran as their dedicated support agent, whom you can reach via phone or email.

If your business needs a reliable way to accept payments from international customers, SecureGlobalPay provides the tools and expertise needed to launch and scale global payment processing.

Sign up with SecureGlobalPay and process payments with peace of mind.

FAQs on international payment processing

Strictly speaking, an international merchant account is a broader term that covers an offshore merchant account. For practical intents and purposes, they are pretty much the same, as both are often used by international businesses or merchants in higher-risk industries.

An international merchant is a business that sells products or services to customers in multiple countries. These businesses typically accept payments in different currencies and use payment processors that support cross-border transactions.

No. In most cases, you can open an international merchant account with a legally registered company in your home country. However, some high-risk industries or global businesses may choose to open an offshore company to access certain banks or payment processors.

To accept international payments, businesses typically need a merchant account, a payment gateway, and a payment processor that supports cross-border transactions. To streamline international transactions, you will also want support for multi-currency payments and alternative payment methods for customers in different regions.

Yes. Some payment providers specialize in working with high-risk businesses and can help them obtain international or offshore merchant accounts. Approval usually requires additional documentation and has higher processing fees, but it also comes with stronger fraud and chargeback controls.