A Guide to Credit Card Processing for High-Risk Merchants (+ Best Providers)

Operating a high-risk business inevitably comes with payment processing obstacles — rejected applications, higher fees, rolling reserves, fund holds, or even sudden account shutdowns.

The easiest way to sidestep those issues is to work with specialized payment processors who can set you up with high-risk credit card processing. You’ll get access to acquiring banks, merchant accounts, fraud tools, and payment infrastructure designed to support your type of business.

Let’s see what credit card processing for high-risk merchants entails, what it costs, and how to find the right provider for your business. At the end, just in case you need it, we’ll also cover alternative payment options for high-risk merchants.

QUICK TAKEAWAYS

- High-risk credit card processing allows businesses in higher-risk industries to accept card payments through specialized merchant accounts.

- High-risk processing typically involves higher fees and stricter terms, but it also gives you stronger fraud and chargeback controls.

- Choosing the right high-risk credit card processing company is essential for fast approval, stable processing, and long-term business growth.

What is high-risk credit card processing?

High-risk credit card processing simply refers to high-risk merchants accepting and processing credit card payments. The “high-risk” classification implies that those credit card transactions carry increased risk, which usually manifests as higher-than-average chargebacks, regulatory oversight, or fraud exposure.

For merchants, that often translates to higher credit card processing fees and more stringent contract terms, such as rolling reserves and limitations on processing volume.

To start accepting card payments as a high-risk business, you’ll typically need a:

- High-risk merchant account: A specialized merchant account approved for high-risk industries.

- PCI-compliant payment gateway: Software that securely transmits payment data from your website or payment system to the processor.

- Payment processor: The company that sets you up with the merchant account and handles transaction routing between your business, the card networks, and the issuing bank.

- Compatible checkout or payment integration: An online checkout page, shopping cart, or POS system that connects to your gateway.

- Fraud and chargeback management tools: Systems that help detect suspicious transactions and reduce chargebacks. They are often built into the payment gateway, but can also come as standalone third-party tools that integrate with it.

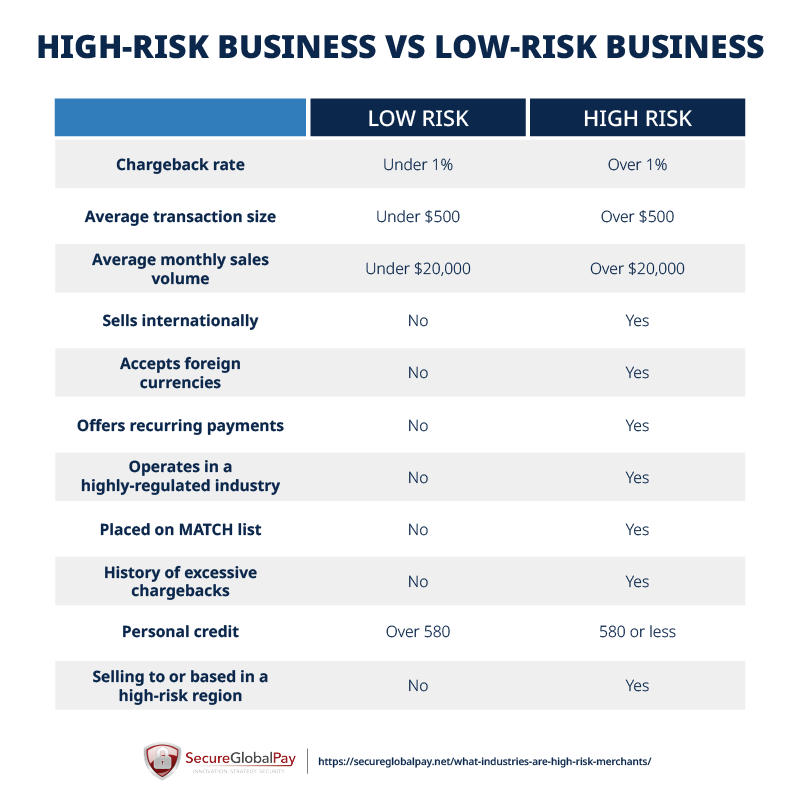

If you’re wondering how banks and processors determine if you are a high-risk business or not, you’re definitely not alone. There are quite a few factors at play — your merchant category code (MCC), type of product/service you’re selling, historical chargeback rates, average transaction size, monthly processing volume, and more.

We created the table below to summarize the most impactful factors in high-risk categorization.

Best high-risk credit card processing companies

Not all payment processors are willing — or equipped — to support high-risk merchants. That’s why it’s important to look for providers that specialize in high-risk industries and have established relationships with acquiring banks that accept these types of businesses.

When searching for a high-risk credit card processing provider, your goal should be to find a long-term partner. Pay special attention to their pricing transparency, the high-risk industries they support, and the responsiveness of their customer support. A capable provider should also offer a reliable payment gateway, flexible integrations, and the ability to scale (e.g., a multiple-MIDs setup) as your transaction volume grows.

Here are a few well-known high-risk credit card processing companies to consider:

- SecureGlobalPay → Best for flexible high-risk merchant accounts and global payment support. SecureGlobalPay specializes in helping high-risk merchants across the US, Canada, the EU, and the UK get approved and set up quickly. You also get a robust payment gateway, fraud-protection tools, transparent pricing, and expert customer support.

- PaymentCloud → Best for personalized onboarding and strong banking relationships. PaymentCloud works with a large network of acquiring banks to help place merchants that may struggle to get approved elsewhere. They also offer good support during the application and initial onboarding processes.

- Durango Merchant Services → Best for offshore and international high-risk businesses. Durango is known for supporting complex and ultra-high-risk industries, working with merchants that have already been declined multiple times, and offering offshore merchant account options.

- Soar Payments → Best for highly-regulated or restricted industries. Soar Payments focuses on compliance-heavy sectors and provides tailored processing solutions and support for merchants in those challenging industries.

If you’re interested in a deeper breakdown with more options, check out our head-to-head comparison of US high-risk merchant account providers.

Free Template for Comparing Merchant Service Providers

Our Google Sheet template arms you with 13 critical questions you should ask each provider to catch red flags and cut through the sales talk — with SecureGlobalPay’s answers already filled in for comparison.

How does high-risk credit card processing work?

At a basic level, high-risk credit card processing works the same way as standard card payment processing.

Here’s what happens when a customer pays with a credit card:

- Customer enters payment details: The customer enters their card information at checkout, either online, through a payment link, or at a point-of-sale terminal.

- Payment gateway encrypts the transaction: The payment gateway securely encrypts the card data and sends it to the payment processor.

- Processor sends the transaction to the card network: The processor forwards the transaction request to the appropriate card network (such as Visa or Mastercard), which then sends it to the customer’s issuing bank.

- Issuing bank approves or declines the payment: The issuing bank verifies the card details, checks available funds, and decides whether to approve or decline the transaction.

- Funds are settled to the merchant account: If the payment is approved, the funds move through the card network and are eventually deposited into the merchant’s account, typically within a couple of business days.

On top of this, for high-risk business credit card processing, providers often add extra protections like:

- Additional monitoring: The processor may flag unusual activity, such as a sudden spike in transaction volume or a large number of purchases from the same IP address.

- Fraud filters: A transaction might be automatically blocked if the billing address doesn’t match the cardholder’s address (AVS mismatch) or if the card fails a CVV verification check.

- Chargeback controls: The processor may alert the merchant when a customer initiates a dispute and provide tools (like chargeback alerts or representment services) to respond before the chargeback escalates.

These safeguards enable high-risk merchants to accept card payments while maintaining a more secure and stable processing environment.

The true cost of high-risk card processing

High-risk merchant accounts come with higher fees than standard payment processing. Banks perceive there is a higher risk of working with such businesses, so they slap on fees to compensate for that additional risk.

While pricing can vary depending on the provider and the type of business, most high-risk merchants can expect a combination of the following costs:

- Setup or underwriting fees: Some providers charge a one-time fee to review and approve the merchant account application and to help with the initial setup.

- Transaction fees: Usually higher than standard processing rates, often ranging from around 2% to 4% per transaction, depending on the industry and risk level.

- Monthly account fees: Some providers charge a monthly fee to maintain the merchant account and payment gateway services.

- Rolling reserve: A percentage of each transaction (often 5–10%) may be temporarily held by the processor to cover potential chargebacks or disputes.

- Chargeback fees: Fees applied when a customer disputes a transaction, typically ranging from $15 to $50 per chargeback.

For a more detailed breakdown, refer to our guide on high-risk merchant account fees.

Although the costs are higher, you also get access to stronger fraud-detection systems, chargeback-prevention tools, and risk-monitoring features. Plus, if you can keep chargebacks low and steadily increase your processing volume, many of those fees are negotiable and can be reduced or eliminated.

QUICK AND EASY ONLINE APPLICATION

We specialize in getting high-risk merchants approved and processing!

Alternative payment processing options for high-risk merchants

If you can’t get approved for credit card processing — or find the fees too high — you still have options. In fact, many high-risk merchants use alternative payment methods either as a backup or to offer customers additional ways to pay.

While these options may not fully replace credit card payments, they can help businesses grow and reduce their dependence on traditional card networks.

Some common alternatives include:

- ACH and eChecks: Both ACH payments and eChecks allow customers to pay directly from their bank account using their routing and account number. They typically have lower processing fees than credit cards and are commonly used for subscriptions, recurring billing, and high-ticket transactions.

- Wire transfers: For large transactions, you can use domestic or international bank wires. Just keep in mind they are not ideal for recurring and everyday purchases.

- Crypto payments: Some high-risk merchants accept Bitcoin and other cryptocurrencies. These payments can settle quickly and reduce the risk of chargebacks, though they are not suitable for every business or customer base.

In many cases, the best approach is to combine multiple payment options. This gives customers flexibility while helping high-risk businesses maintain consistent cash flow even if credit card processing becomes limited or temporarily unavailable.

SecureGlobalPay offers both high-risk credit card processing and alternative options like ACH and eCheck payments, allowing merchants to diversify how they accept payments. This helps reduce processing disruptions and lower costs on certain transactions.

Choose a high-risk provider that can help you scale

SecureGlobalPay is a merchant service provider that works with a wide range of high-risk merchants, helping them accept and process credit card payments reliably while maintaining strong fraud and chargeback controls.

Here’s what we can do for you:

- High-risk merchant accounts supported by acquiring banks that work with your industry and business model.

- Robust, PCI-compliant payment gateway with hundreds of integrations that simplify online payments, recurring billing, customer management, and reporting.

- Advanced fraud and chargeback management tools to help protect revenue and maintain healthy processing ratios.

- Dedicated support from high-risk payment specialists who understand the challenges these businesses face.

- Transparent, integrachange-plus pricing and scalable solutions that grow alongside your business.

If you’re looking for a reliable payment partner that understands the needs of high-risk merchants, SecureGlobalPay can help you get started quickly and process payments with confidence.

Sign up today using our simple online application.