All You Need to Know to Secure the Best High-Risk Merchant Account

High-risk merchant accounts offer a lifeline for businesses that struggle to secure traditional merchant services because of the nature of their business, higher chargeback rates, or other risk factors.

If your business falls into the high-risk category, you need to know what that categorization means and how it impacts your ability to accept and process payments.

This guide will give you a concise overview of how a high-risk merchant account works — from criteria and operational differences to the challenges and fees involved. Plus, we’ll provide practical advice on securing the best high-risk merchant account contract and have a quick look at the most popular providers.

Whether you’re a brand-new business or looking to switch providers, we’re here to help you navigate the high-risk merchant landscape.

QUICK TAKEAWAYS

- A high-risk merchant account is tailored for businesses deemed higher risk and comes with higher fees, stricter terms, and added safeguards like rolling reserves.

- Business are considered "high-risk" based on factors like their chargeback ratio, risk of fraud, industry type, and their business model.

- Opening and setting up a high-risk merchant account usually takes a week or longer, due to more extensive underwriting procedures.

- High-risk merchant should look for specialized providers like SecureGlobalPay, that offer industry experience, clear pricing, robust chargeback and fraud tools, and excellent customer support.

What is a high-risk merchant account?

A high-risk merchant account is a specialized payment processing account designed for businesses that pose a higher risk to the sponsoring bank, financial institution, and payment processor offering merchant services.

Unlike regular merchant accounts, which are readily available to most retail businesses, high-risk accounts come with unique considerations and requirements due to the potential likelihood of chargebacks and fraud.

The key difference between a high-risk and a standard merchant account lies in their terms and conditions. High-risk accounts often come with higher processing fees, more stringent contract terms, and sometimes require rolling reserves as a financial safeguard for the provider.

That being said, high-risk merchant accounts come with some benefits as well: advanced security measures, higher chargeback thresholds, value-added services for chargeback mitigation, and the ability to sell high-risk products or services.

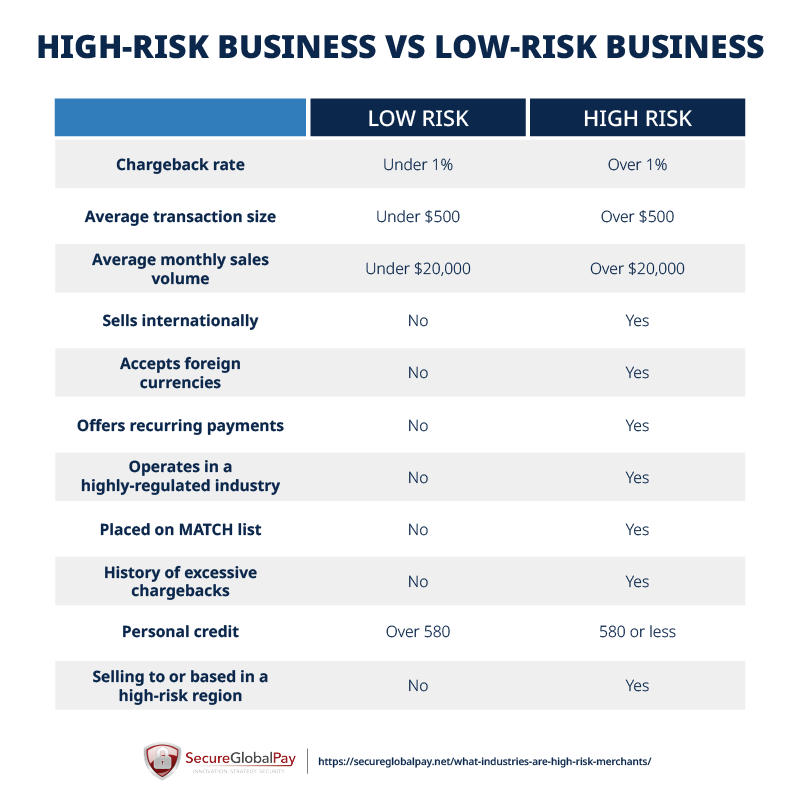

What makes a business high risk?

Several factors contribute to a business being classified as high risk in the eyes of merchant account providers and financial institutions. Here are the most common ones:

- Industry reputation: Certain industries are inherently considered high risk due to their higher likelihood of chargebacks and fraud. Examples include adult entertainment, e-cigarettes and vaping, CBD, firearms, travel, tobacco, and high-risk ecommerce.

- Financial stability: Businesses that have a history of financial instability, poor credit, or are new with an unproven track record are often seen as high risk.

- High chargeback rates: Companies experiencing high levels of chargebacks are flagged as high risk because chargebacks can be an indicator of unsatisfied customers or fraudulent activity.

- International sales: Businesses that deal with international sales face higher risks due to different laws, currencies, and the potential for fraud.

- Subscription-based models: Companies that operate on a subscription or recurring billing model are at a higher risk for chargebacks, as customers sometimes dispute these charges.

- High-risk markets: Operating from or in nations considered to be high-risk markets can be a red flag. Best examples are countries in Africa and Southeast Asia that are known safe havens for fraudsters, with poor business and banking practices.

While the exact evaluation methods and criteria vary slightly from provider to provider, if you fall into one of these categories, you’re likely going to need a high-risk merchant account.

All of these factors underscore the importance of understanding and managing the risks associated with high-risk merchant accounts, as well as partnering with a provider that can help you manage any arising issues.

As a qualified high-risk merchant services provider that has been doing this for almost 30 years, the SecureGlobalPay team knows exactly what it takes to get you approved.

SIGN UP WITH SECUREGLOBALPAY

We specialize in getting high-risk merchants approved and processing!

Do I need a high-risk payment gateway in addition to a merchant account?

If you plan to process credit card payments as a high-risk merchant — yes, you’ll need both. While your merchant account holds and settles the money, the gateway is what makes the transaction happen in the first place — especially for online payments.

If you can, it’s best to get both your high-risk merchant account and payment gateway from the same provider. This way, you’ll have:

- Smoother setup: Everything is pre-integrated; your merchant account provider can tell you exactly which integrations their payment gateway supports and how they work.

- Fewer technical issues: Connecting systems from different providers leaves more room for technical problems.

- Faster support: One company handles everything; you won’t end up in a never-ending finger-pointing circle when an issue arises.

- Better performance: Since the provider works with high-risk merchants, you are more likely to get access to a gateway with robust security, fraud, and chargeback tools.

That said, you can have your merchant account with one company and your payment gateway with another. In that setup, the gateway integrates with your merchant account, sending transaction data back and forth so payments can be processed normally.

Be careful — not all gateways are compatible with all high-risk merchant accounts. Before choosing a provider, always double-check that the gateway works with your business model (like subscriptions, in-app payments, or multi-currency international transactions). A little due diligence here can save you from major headaches later.

The costs of a high-risk processing merchant account

The costs associated with high-risk processing are typically higher than those for retail merchants. The fees are structured to cover the additional risk and operational costs involved in monitoring and securing high-risk transactions.

Here is a quick breakdown of the typical fees involved:

- Setup fees: Some providers will charge a fixed one-time fee to help set up your account.

- Transaction fees: Each transaction may incurs processing fee, that scales based on your industry and perceived level of risk.

- Monthly or annual fees: Some high-risk accounts have monthly or annual account fees to maintain the account.

- Rolling reserve fees: The funds held in rolling reserves are not immediately available to the merchant, which can affect cash flow. While not a direct fee, this practice has financial implications for the business.

- Chargeback fees: If a chargeback occurs, the fees associated with it are usually higher for high-risk accounts, given the increased administrative costs of handling disputes.

- Premature termination fees: If you sign a long-term contract, some payment processors will charge hefty fees for early termination of that contract.

- PCI compliance fees: Maintaining compliance with the Payment Card Industry Data Security Standard (PCI DSS) is crucial for all businesses that handle credit card information. apply to standard merchant accounts as well. By being aware of the increased scrutiny and costs involved, businesses can better prepare and manage their operations to mitigate risks and maintain financial stability.

For a more detailed breakdown, check out our guide to high-risk merchant account fees and rates.

10 Best high-risk merchant account providers

Here are some of the top high-risk merchant account providers worth considering:

- SecureGlobalPay: Works with a wide range of industries and provides both domestic and offshore accounts. It’s led by a smaller team of industry veterans and recognized for its quick and helpful support. Great all-around option.

- PaymentCloud: Known for high approval rates and strong support, especially for businesses that have been declined elsewhere.

- Durango Merchant Services: A long-standing high-risk specialist with global processing options and support for a wide range of industries.

- Soar Payments: Focused on eCommerce and subscription businesses, with transparent pricing and solid customer service.

- Host Merchant Services: Offers both low- and high-risk accounts with competitive pricing and good flexibility.

- Instabill: Strong international capabilities and support for offshore merchant accounts.

- PayKings: Known for working with harder-to-place businesses and offering tailored solutions.

- eMerchantBroker: One of the more established names in high-risk processing, with a wide range of supported industries.

- High Risk Pay: Focuses on fast approvals and simple onboarding for high-risk merchants.

- CCBill: A go-to option for subscription-based and adult businesses, with built-in billing tools.

Again, for more details, read our comparison of popular US high-risk merchant services providers.

Now, let’s see how to choose between these options and find the right solution for your business.

How to evaluate merchant services providers for your high-risk business

Be sure to properly research any provider you’re considering. We highly recommend jumping on a call and discussing details with their business representative. This will help you estimate how helpful/responsive their support is and get answers to these critical questions.

Pay close attention to the following factors during the vetting process:

- Industry experience: Make sure the payment provider has experience working with business models in your industry.

- Account manager: Ensure an open line of communication with a seasoned professional who cares about your success. Having a dedicated account manager who will return phone calls and emails in a timely manner is of utmost importance.

- Iron-clad security: Confirm if there is an unfailing and multi-layered chargeback system in place. AI-based checks, real-time notifications, and anti-fraud tools are also mandatory.

- Track record: How long has the high-risk credit card payment provider been around? What experience do they have in handling high-risk merchant accounts like yours?

- Features: Does the high-risk payment provider allow you to use multiple merchant accounts on a single payment gateway? Is it possible to customize your payment order page? Do they provide ACH payment services? Do you have 100% control of your setup and payment process?

- Technology: The best providers will be able to offer you (POS) point-of-sale systems, virtual terminals, mobile payment solutions, credit card terminals, payment gateways with shopping carts, and different website integrations.

- Adaptability: Choose a high-risk merchant account provider that allows you to alter your payment scenarios as the need arises. Discuss rates, fees, and business conditions.

- Customer support: Select a provider that knows the importance of customer service. 24/7 support, training, troubleshooting, and maintenance are important to the sustainability of your business. You’ll want someone who can respond quickly if you’re having issues with accepting credit card payments on your website.

- Contract length: Avoid companies that offer long-term contracts. Many high-risk merchant account service providers lock merchants in lengthy contracts with an automatic renewal clause and an early termination fee.

- Clear pricing: Your payment processor should be able to provide clear and transparent pricing and explain all of the costs involved.

The final point about pricing is extra important. The pricing should always be listed on the acquiring bank application or readily provided when you ask for it. After this, there should be no further surprises or hidden charges.

If the information you are asking for falls short or is incomplete, look for a different provider.

Free Template for Comparing Merchant Service Providers

Our Google Sheet template arms you with 13 critical questions you should ask each provider to catch red flags and cut through the sales talk — with SecureGlobalPay’s answers already filled in for comparison.

The information you’ll need to provide to apply for a high-risk merchant account

Opening a high-risk merchant account is a bit more involved than a standard one. Providers take a closer look at your business because they’re taking on more risk — which translates to a few additional documents and information you’ll need to submit.

Here’s what you’ll typically need to provide:

- Basic business details: Legal business name, address, contact info, and registration documents.

- Business license (if applicable).

- Owner/Director information: IDs, personal details, and sometimes a credit check.

- Bank account details (where your funds will be deposited).

- Processing history: Previous merchant statements (usually the last 3–6 months) if you’ve processed payments before.

- Projected sales volume: Expected monthly revenue, average transaction size, and max ticket size.

- Website information: Link to your live site, including product/service details, terms & conditions, privacy policy, and refund policy.

- Chargeback history (if applicable, including past ratios and issues).

- Fulfillment details: How and when customers receive your product or service.

Depending on your industry, you might also be asked for extra documentation — think compliance certificates, licenses, supplier agreements, and similar.

In the application process, the more information you can provide, the more streamlined the process will be. Based on your existing processing history and income, merchant services providers can offer various pricing options that are a good match for your business model.

If your merchant account application is denied, that doesn’t mean you are without options. Call a SecureGlobalPay customer service representative to get more info. We have the experience you need to navigate the application process and will work to find a customized solution for your situation.

Open a high-risk merchant account at SecureGlobalPay

SecureGlobalPay is a merchant service provider that works with a wide range of high-risk industries, helping businesses accept and process payments reliably while maintaining strong fraud and chargeback controls.

Here’s what we can do for you:

- High-risk merchant accounts supported by acquiring banks that work with your industry and business model.

- Robust, PCI-compliant payment gateway with hundreds of integrations that simplify online payments, recurring billing, customer management, and reporting.

- Advanced fraud and chargeback management tools to help protect revenue and maintain healthy processing ratios.

- Dedicated support from high-risk payment specialists who understand the challenges these businesses face.

- Transparent, integrachange-plus pricing and scalable solutions that grow alongside your business.

Learn more by sending a question to partners@secureglobalpay.net or by filling out our online application form.

Frequently Asked Questions

A high-risk account refers to a merchant account designated for businesses that operate within specific industries or have business models that financial institutions and payment processors consider to carry a higher risk of chargebacks, fraud, or regulatory issues.

This classification can be due to various factors, including the business’s industry, financial history, sales volume, and the countries they serve. High-risk accounts often come with stricter terms and higher fees to offset the increased risk to the provider.

The rates for high-risk merchant accounts vary by provider, specific risk factors, and the services offered. Most high-risk businesses can expect their processing rates to be somewhere between 2% and 6%.

A high-risk transaction is one that presents a higher likelihood of chargeback, fraud, or non-compliance with payment industry standards. Factors that may categorize a transaction as high risk include the transaction’s size, the type of product or service being sold, transactions that involve recurring payments, sales in countries with high levels of fraud, and any transactions that do not adhere to the payment processor’s standards for secure and legitimate business practices.

Costs are higher than standard accounts because the provider is taking on more risk. You can expect higher processing fees (often a few percentage points more per transaction), plus possible setup fees, monthly fees, and account reserves. Exact pricing varies based on your industry, chargeback history, and volume — but the riskier you are on paper, the more you’ll typically pay.

A high-risk LLC is simply a business registered as an LLC that operates in a high-risk category. This could be due to the industry (like supplements, adult, gaming, or travel), or because of factors like high chargebacks, large transaction sizes, or selling internationally. It’s not about the LLC structure itself — it’s about how and where the business operates.

An inherently high-risk business is one that’s almost always considered risky due to its industry, like CBD, adult content, or gambling. These businesses will nearly always need a high-risk merchant account.

A conditionally high-risk business isn’t risky by default but becomes high-risk based on certain factors, like high chargeback rates, poor credit history, or unusual sales patterns. For example, a regular eCommerce store could be labeled high-risk if it has too many disputes or sudden spikes in volume.

Not really. While some providers advertise “fast approvals,” true instant approval is impossible in the high-risk space due to an extensive underwriting process, which takes anywhere from a couple of days to a week (sometimes longer for complex cases).

The best way to improve your chances is to come prepared and present your business clearly. Make sure your website is functional and transparent, keep your chargebacks as low as possible, and provide accurate information during the application.

Working with a provider that specializes in your industry also helps a lot. They can provide you with expert advice and have pre-existing relationships with acquiring banks that support your industry and business model.