Home » How to Get a Merchant Account With Bad Credit in 2026

How to Get a Merchant Account With Bad Credit in 2026

| June 16, 2026

Opening a bad credit merchant account can be challenging. If your personal credit, business credit, or past payment history raises concerns, traditional banks and processors immediately start to worry about unpaid fees, chargebacks, and fraud losses.

The good news is that poor credit does not have to stop you from accepting payments. Your best option is to work with an experienced high-risk merchant account provider like SecureGlobalPay. We understand how underwriters evaluate bad-credit applications and work with acquiring banks that are more open to hard-to-place merchants.

In this quick guide, we will explain how payment processors define bad credit, where to apply for a merchant account with poor credit, and how to improve your chances of approval.

QUICK TAKEAWAYS

- Bad credit can make merchant account approval harder, but it does not mean automatic denial.

- High-risk merchant account providers are usually a better fit than standard payment facilitators for bad-credit merchants.

- Preparing documents, explaining credit issues, and presenting a risk mitigation plan can improve your approval odds.

- SecureGlobalPay helps hard-to-place merchants get approved through experienced underwriting support and acquiring bank relationships.

What is considered “bad credit”?

In payment processing, bad credit refers to a personal or business credit history that suggests a higher likelihood of financial problems, such as missed payments, defaults, collections, or bankruptcies.

Merchant account providers review credit reports to evaluate how reliably you have managed debt and financial obligations in the past, which helps them estimate the risk of future losses related to chargebacks, fees, or account balances.

There is no universal cutoff because every processor and acquiring bank uses its own underwriting rules. Broadly speaking, if your credit score is below 600, you’ll have much better chances with a high-risk merchant account provider.

Here’s how standard FICO Score ranges impact merchant account approval:

| Credit score range | Rating | Likely impact on merchant account approval |

| 800–850 | Exceptional | Strong approval odds and better terms |

| 740–799 | Very good | Strong approval odds with standard terms |

| 670–739 | Good | Still acceptable for most processors |

| 580–669 | Fair | May trigger extra review, higher pricing, or reserves |

| 500-580 | Poor | Often treated as high risk, with stricter terms |

| Below 500 | Very poor | Approval becomes extremely difficult |

In practice, underwriters look beyond your score. They may also review:

- Business type or industry risk: Some industries are automatically considered higher risk.

- Prior bankruptcies, liens, collections, or unpaid processor balances: These can raise concerns about future losses.

- Chargeback history: A high chargeback rate can make approval harder.

- Processing volume and average ticket size: Higher volume or larger tickets can increase risk.

- Time in business: Newer businesses may face more scrutiny.

- Cash flow, bank statements, and reserves: Strong cash flow can help offset weak credit.

- Personal guarantee: Most processors will require the owner to personally guarantee the account.

Bad credit does not mean automatic denial. However, your account may start with limits such as rolling higher processing fees, rolling reserves, lower monthly volume caps, or delayed funding.

These restrictions are rarely permanent. If you process consistently, keep chargebacks low, and build a clean payment history, you should be able to renegotiate better contract terms down the line (usually within 3 to 9 months).

Steps for opening a merchant account with bad credit

If you have low credit, applying through a standard payment facilitator (like Stripe or PayPal) is risky. PayFacs are built for fast onboarding, but they often rely on automated risk checks, broad approval rules, and post-approval monitoring.

That means your account may be approved quickly, then frozen or closed later if your risk profile triggers a review.

To avoid stressful processing issues and improve chances for approval, bad-credit merchants should open a high-risk merchant account. The process looks like this:

- Find a high-risk merchant account provider: Look for a provider that works with bad-credit merchants, high-risk industries, chargeback-prone businesses, and hard-to-place accounts.

- Fill out an online application: Prepare and submit your business license, owner ID, bank statements, processing statements, voided check, website URL, and any other requested documents.

- Submit the application for underwriting: Your provider will send your file to an acquiring bank or processor that is willing to review bad-credit merchant applications.

- Review the proposed terms: Look carefully at processing rates, monthly fees, reserves, volume caps, funding timelines, contract terms, and chargeback rules.

- Set up your payment gateway: Once approved, configure your gateway, fraud prevention tools, payment methods, checkout page, and integrations.

Free Template for Comparing Merchant Service Providers

Our Google Sheet template arms you with 13 critical questions you should ask each provider to catch red flags and cut through the sales talk — with SecureGlobalPay’s answers already filled in for comparison.

How to improve your approval odds and speed up the process

Getting approved with bad credit is easier when you make the underwriter’s job simple. The goal is to show that your business is real, your payment risk is manageable, and you are prepared to operate responsibly.

The more complete your application is, the faster your provider can match you with the right acquiring bank. Small details matter — missing documents, unclear policies, or unexplained credit issues can slow the process or lead to stricter terms.

1. Prepare your documents before you apply

Before you apply, gather the documents underwriters need to review your business. A complete file helps your high-risk merchant account provider move faster and gives the acquiring bank fewer reasons to pause the application.

Commonly requested documents include:

- Government-issued ID: Used to verify the business owner’s identity.

- Business license or registration: Confirms that your business is legally registered.

- EIN or tax ID: Helps verify your business for tax and underwriting purposes.

- Bank statements: Shows cash flow, account stability, and available reserves.

- Processing statements: Shows your sales volume, chargeback history, refund activity, and average ticket size.

- Voided check or bank letter: Confirms where settlement funds should be deposited.

- Website URL: Allows the underwriter to review your products, policies, pricing, and checkout flow.

- Financial statements: May be requested if your business has high volume, high tickets, or a complex risk profile.

If a document is missing or outdated, fix it before you apply. Clean, current paperwork can make a bad-credit application look more organized and lower risk.

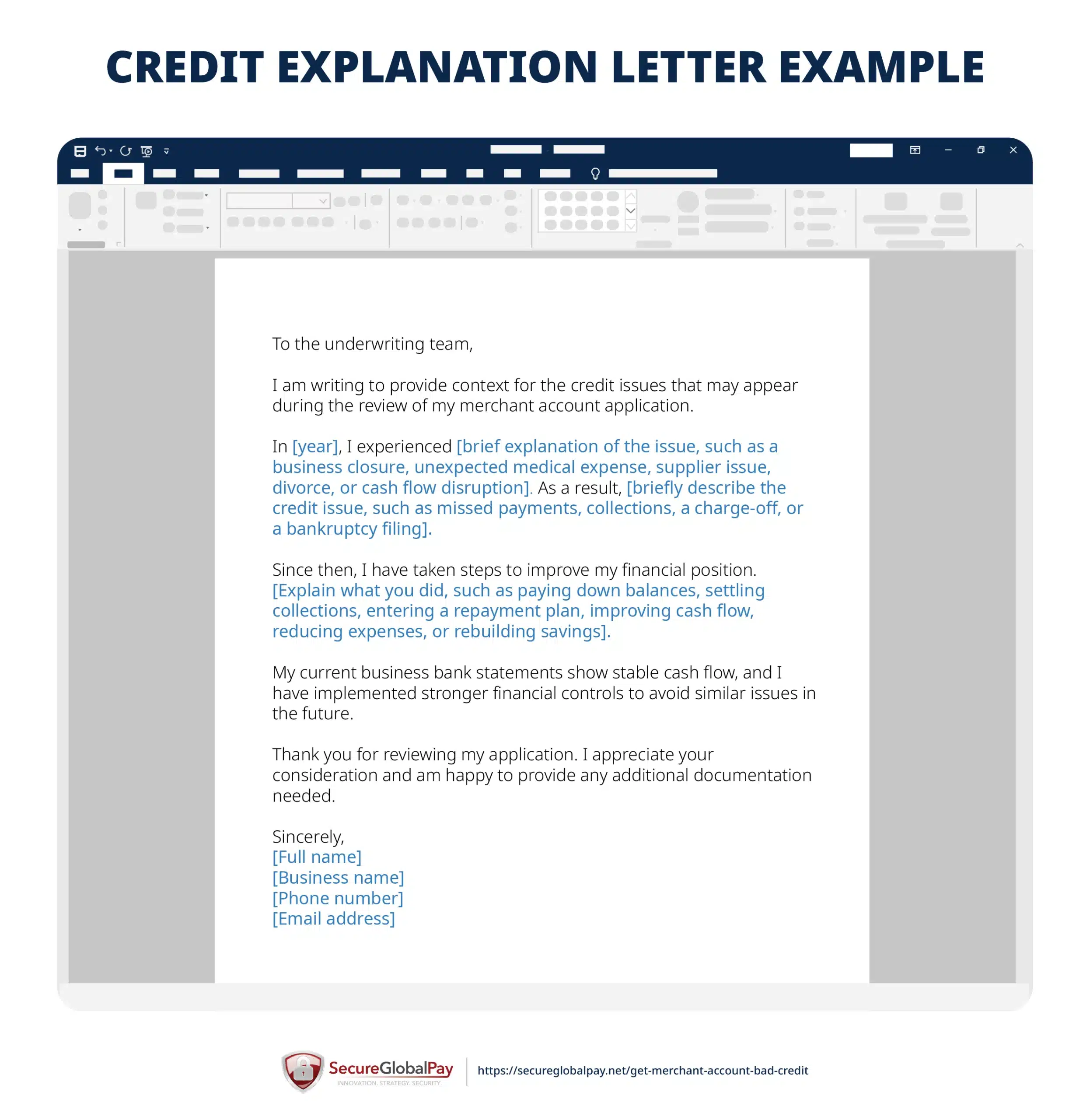

2. Include a credit explanation letter

Do not ignore past credit issues or hope the underwriter will overlook them. It is better to address bad credit upfront and explain the situation on your terms.

Be short, honest, and specific. Explain what happened, why it happened, and what you have done to reduce the risk of the same problem happening again.

Keep the tone professional and factual. Underwriters do not expect a perfect credit history, but they do want to see that you understand the issue and have a plan to manage risk going forward.

3. Clean up your website and checkout flow

Your website is part of the underwriting review. If your site is confusing and has a bunch of broken elements, the processor may slow down the application, ask for changes, or decline the account.

Before you apply, make sure your website clearly shows what you sell, how customers pay, and how customers can contact you if there is a problem. A clean website and checkout flow can make your business look more legitimate and lower risk.

At a minimum, review these areas before submitting your application:

- Product or service descriptions: Explain exactly what customers are buying.

- Pricing: Show clear prices, fees, billing terms, and subscription terms.

- Refund and cancellation policy: Make your refund rules easy to find and understand.

- Shipping and fulfillment policy: Explain delivery timelines, tracking, and fulfillment expectations.

- Terms of service: Outline customer responsibilities, business policies, and purchase conditions.

- Privacy policy: Explain how customer data is collected, used, and protected.

- Contact information: Include a working phone number, email address, and business address if applicable.

4. Present a risk mitigation plan

A risk mitigation plan shows the underwriter that you understand the main risks in your business and have a clear plan to manage them. This is especially helpful if you have bad credit, past chargebacks, high ticket sizes, or limited processing history.

This plan does not need to be long. It should focus on the risks that matter most to payment processors, such as chargebacks, fraud, refunds, fulfillment delays, and cash flow.

A strong risk mitigation plan can make your application feel more complete and credible. It gives the underwriter a reason to see your business as managed risk, not uncontrolled risk.

5. Offer a merchant account reserve

A merchant account reserve is a portion of your processing funds that the processor holds to cover possible chargebacks, refunds, unpaid fees, or other losses. Some acquirers will be more likely to accept a merchant who has poor credit if they know that they are open to some sort of reserve.

A reserve is not ideal for cash flow, but it can be a practical tradeoff if your credit profile makes approval harder. If you process consistently and keep risk low, you should be able to request better terms later.

6. Start with realistic processing volume

Asking for a very high monthly processing limit can trigger a decline. If your credit is weak, underwriters want to see that your requested volume matches your current sales, bank statements, and business history.

So, start with a realistic limit based on what you can support today. After you build a clean processing history, you can request a higher limit.

If you are continusosly exceeding your monthly volume processing cap, SecureGlobalPay can set you up with multiple MIDs and keep all accounts healthy and under the approved processing threshold through load balancing and intelligent payment gateway routing.

7. Pay down urgent debt or collections first

Open collections, unpaid processor balances, tax liens, and other urgent debts will negatively impact your approval odds. Underwriters view unresolved debts as a sign that your business could struggle to cover processing fees, refunds, or chargebacks.

Just showing progress can help. Even partial repayment, a settlement agreement, or a documented payment plan can make your application stronger.

If you cannot pay everything before applying, be ready to explain what happened and show what you are doing to fix it. This could, for example, be included in (or alongside) your credit explanation letter we discussed earlier.

8. Highlight stable cash flow

Stable cash flow can help offset weak credit because it shows the underwriter that your business can cover all of its financial obligations. Even if your credit score is low, healthy bank statements can make your application look less risky.

If your cash flow has recently improved, point that out in your application.

9. Fix errors on your credit report

Credit report errors can make your application look worse than it really is. Before you apply, review your personal and business credit reports.

If you find an error — incorrect balances, duplicate accounts, outdated negative items, or accounts that do not belong to you — dispute it with the credit bureau or reporting agency. You should also keep records of the dispute in case the underwriter asks for more context.

You can get free weekly credit reports from the three major credit bureaus through AnnualCreditReport.com. If you identify inaccurate information, the Consumer Financial Protection Bureau explains how to file a credit report dispute.

10. Consider a co-signer or a stronger guarantor

If your personal credit is the main problem, adding a financially stronger owner, partner, or guarantor may improve your chances. This option is not available with every processor, and it should not be taken lightly.

Before you apply with a co-signer or guarantor, make sure everyone understands the responsibility. The underwriting team may review the guarantor’s credit, financial history, and ownership role before making a decision.

11. Respond quickly to underwriting requests

Underwriting can move faster when you respond to document requests, questions, and follow-ups quickly. If the processor asks for more information, the request usually means the application is still being reviewed — not that you have been declined.

Delays can create doubt or push your file to the bottom of the queue. A fast, organized response helps show that you are serious, prepared, and easy to work with.

To keep the process moving:

- Check your email often: Watch for messages from your provider, processor, or acquiring bank.

- Send complete documents: Provide every requested page in the right format, not just screenshots or partial files.

- Keep file names clear: Use simple names like “March 2026 bank statement” or “Business license.”

- Answer questions directly: Give short, specific answers instead of vague explanations.

- Be consistent: Make sure your answers match your application, website, and bank statements.

- Ask for clarification: If you do not understand a request, ask your provider what the underwriter needs.

The easier you make the review, the better your chances of a smooth approval process.

Get a bad credit merchant account from SecureGlobalPay

Bad credit can make merchant account approval harder, but the right provider can make the process much easier. SecureGlobalPay is an all-in-one merchant services provider that helps high-risk and hard-to-place merchants get approved and processed.

Our long-standing relationships with acquiring banks help us place applications with partners that understand higher-risk accounts and are willing to onboard merchants with low credit scores.

When you work with SecureGlobalPay, you get:

- Domestic and international merchant accounts: Accept payments through processing solutions that fit your business model, location, and risk profile.

- High-risk expertise: Work with a provider that understands complex underwriting and hard-to-place applications.

- Payment gateway with strong fraud prevention tools: Reduce risk with security tools designed to help protect your account.

- 200+ integrations: Connect your payment setup with chargeback tools, CRM platforms, invoicing software, shopping carts, and other business systems.

- Transparent and competitive pricing: Clear terms with no hidden setup or account cancellation costs. Interchange-plus pricing built around your business needs.

- Dedicated support: Get help with onboarding, underwriting, gateway setup, and ongoing account management.

Sign up with SecureGlobalPay today and get a long-term processing partner that will always have your back.

FAQs

No, you do not always need good credit to get a merchant account. Bad credit can make approval harder, but many high-risk merchant account providers work with merchants who have poor credit, limited credit history, or a history of financial issues.

Yes, you can usually start an LLC if you have bad credit. Forming an LLC is separate from getting approved for financing, banking, or payment processing, although your personal credit may still be reviewed when you apply for a merchant account.

Yes, bad-credit merchant accounts may come with stricter terms. Common restrictions include higher processing fees, rolling reserves, lower monthly volume caps, delayed funding, stricter chargeback monitoring, and more documentation requirements. Most of those restrictions can be eased off if you build up a good track record.

Opening a merchant account with poor credit usually comes with higher processing fees than a standard retail merchant account. But that is a reality for every high-risk merchant. Processors and banks charge higher rates because they see the account as higher risk.

Yes, in many cases, you will be able to renegotiate your merchant contract after improving your credit score and building a clean processing history. If your current provider is not willing to give you better terms despite that, you can always shop around and switch merchant services.

Yes, you may be able to get a merchant account after bankruptcy, but approval depends on how recent the bankruptcy was, your current cash flow, your business model, and your overall risk profile.

Yes, you can get a merchant account with no credit history, but the processor may ask for more documentation, a personal guarantee, lower starting volume, or a reserve.

A merchant account application may involve a credit check, but the impact depends on whether the processor performs a soft inquiry or a hard inquiry. A soft inquiry does not affect your credit score, while a hard inquiry may cause a small, temporary score drop. Ask your provider how they review credit before you apply.

Written By

R

Roland G. Szasz

Director of Business Development at SecureGlobalPay

Roland has spent nearly three decades helping businesses navigate the complexities of payment processing. He now works closely with high-risk merchants that have been declined or restricted by conventional providers - and shares his experience and best practices on this blog.

Tailored payment solutions for high-risk merchants

- Domestic and offshore accounts

- Competitive, interchange plus pricing

- No long-term contracts or hidden fees

- Built in fraud protection

- Dedicated account manager; 24/7

Sign up in 5 minutes

A+ Rating

as of 06/17/26

Related Posts

![Shopify High-Risk Payment Processors in 2026 [Reviewed & Ranked]](https://secureglobalpay.net/wp-content/uploads/Shopify-1-300x158.jpg "Shopify High-Risk Payment Processors in 2026 [Reviewed & Ranked]")