Getting a High-Volume Merchant Account and Payment Processing

A high-volume merchant account is designed for businesses that process a large number of transactions or high dollar amounts each month.

These accounts are tailored to handle the increased risk and complexity that comes with high sales volumes. To keep your business running smoothly, this type of account offers specialized support, lower transaction fees, and better fraud protection.

If you’re looking for a high-volume merchant account with a trusted merchant account provider, fill out our merchant application form after clicking on the image below:

QUICK AND EASY ONLINE APPLICATION

Accept Volume Without Restrictions Now!

If you’re just looking to learn how high-volume payment processing works, what the application process looks like, and some general tips on managing such accounts, continue below.

QUICK TAKEAWAYS

- High-volume merchant accounts are tailored for businesses processing over $100,000 monthly.

- High-risk high-volume accounts involve stricter terms, including higher fees and increased reserves, due to the elevated risks associated with such transactions.

- In turn, they come with higher processing limits and enhanced fraud protection.

- SecureGlobalPay provides specialized high-volume processing solutions, including competitive fees, robust security, and scalable support to grow with your business.

Types of high-volume merchants accounts

Typically, a business must process at least $100,000 per month in credit card & debit card sales to be eligible for a high-volume merchant account.

Here are the most common types of businesses to which we provide high-volume merchant accounts:

- Property management processing & monthly rental payments or timeshare fees

- Merchants charging recurring annual or monthly fees for services

- Subscription merchant account for coaching companies that ship products monthly or bi-monthly

- Businesses selling high-ticket items like coaching programs

- Companies with recurrent membership fees

- Online businesses selling single downloads of songs or e-books

It doesn’t matter if you’re processing a few large transactions or a bunch of micro-payments per day — as long as you hit the required monthly threshold, you can request a high-volume merchant account.

The limits on high-volume payment processing

When you sign up for a standard merchant account, in most cases, your monthly transaction limit will be set between $2,000 and $10,000.

If you occasionally or consistently process past your transaction limit, your funds might be placed on hold. Sometimes, your merchant account might even be suspended pending an inquiry from your processor.

This doesn’t mean you’re being punished for being successful. These limits are a way for merchant service providers to discourage fraudulent merchant accounts.

Oftentimes, scammers will set up and use a merchant account to run massive charges with stolen credit cards. When the merchant account starts getting hit with chargebacks, scammers shut down their account and create a new one.

That is why the processing limit is necessary. It helps the providers of high-volume payment processing to protect themselves and the consumers from all the damage that can be done by an account with no transaction processing limits.

The benefits of having a high-volume merchant account

High-volume merchant accounts come with many distinct benefits:

- Lower transaction fees: With higher volumes, you can often negotiate better terms and rates with your payment processor.

- Higher processing limits and scalability: These accounts are designed to grow with your business, offering flexibility and scalability as your transaction volume increases.

- Enhanced fraud protection: High-volume accounts typically include advanced fraud detection and prevention measures, protecting your business and customers.

- Improved cash flow: Faster processing and settlement times mean quicker access to funds, enhancing your business’s cash flow.

- Dedicated support: Access to specialized customer service teams who understand the unique needs of high-volume merchants, providing faster and more effective support.

In other words, with a high-volume merchant account, you are receiving the maximum amount of processing volume with the maximum amount of security — at the best price and service possible.

How to apply for a high-volume merchant account

First, have a serious conversation with your preferred payment service provider about high-volume payment processing and confirm they can properly manage the relationship. Always be upfront about your volume requirements, average transaction size, and highest estimated ticket.

If you have challenges with your existing merchant services provider and are inquiring about extra volume and bandwidth, ensure you can access your processing statements for the last three months. SecureGlobalPay’s online application will quickly walk you through the steps and guide you toward fast approval.

Once your application is received, a relationship manager will contact you directly to help streamline the approval process and discuss various options regarding multiple merchant account payment processing and transaction routing. Typically, you’ll be asked to provide the following documents:

- Business license: Proof of your business registration.

- Bank statements: Typically, the last three months of statements.

- Financial statements: Profit and loss statements, balance sheets.

- Processing history: Records of previous credit card processing (if applicable).

- Tax ID and EIN: Your business and employer identification numbers.

- Personal identification: A copy of your government-issued ID.

If approved, you’ll receive your merchant account details and can start processing payments.

Now, keep in mind that payment services providers have rules that they must follow before they can approve you for a high-volume merchant account. If you don’t get approval on your first try, you’ll have to focus on:

- Building a strong relationship with your merchant account provider

- Continue building a positive transaction history

- Keep chargebacks low (or look for ways to reduce them)

Doing all this will significantly increase your chances of being approved the next time you apply.

How to manage high-volume transactions and increase processing limits

Businesses can request an increase in their merchant account limits once they surpass their pre-set limits. For example, if you have a monthly volume cap of $80,000, when you pass that threshold, it is normal to request an increased limit of $120,000 or $160,000.

Here are some important things to keep in mind when you request a limit increase:

- Industry type: Certain industries are considered higher risk, like travel or e-commerce, which can affect your chances of approval. In general, low-risk industries are more likely to get approval for limit increases.

- Method of payment: The types of payments you accept (credit cards, ACH, etc.) influence the risk assessment. Businesses that accept a variety of payment methods might have better chances.

- Business credit score: A higher business credit score indicates reliability and lower risk, making it easier to get a limit increase.

- Business processing history: A history of consistent processing without excessive chargebacks or fraud flags shows stability, improving your chances.

- Reasons behind the increase: Clear, logical reasons for needing a higher limit (like seasonal sales spikes or business growth) will help your case.

- Recurrent billing: If you have a high rate of chargebacks from recurrent billing, it might hinder your chances.

- Business banking balance: Maintaining a healthy monthly business account balance demonstrates financial stability, which is a positive indicator for approval.

How does a high-risk high-volume merchant account work

Not all high-volume merchant accounts are considered high-risk, but many fall into this category due to the nature of their business operations. The bigger your processing volume, the more risk it carries.

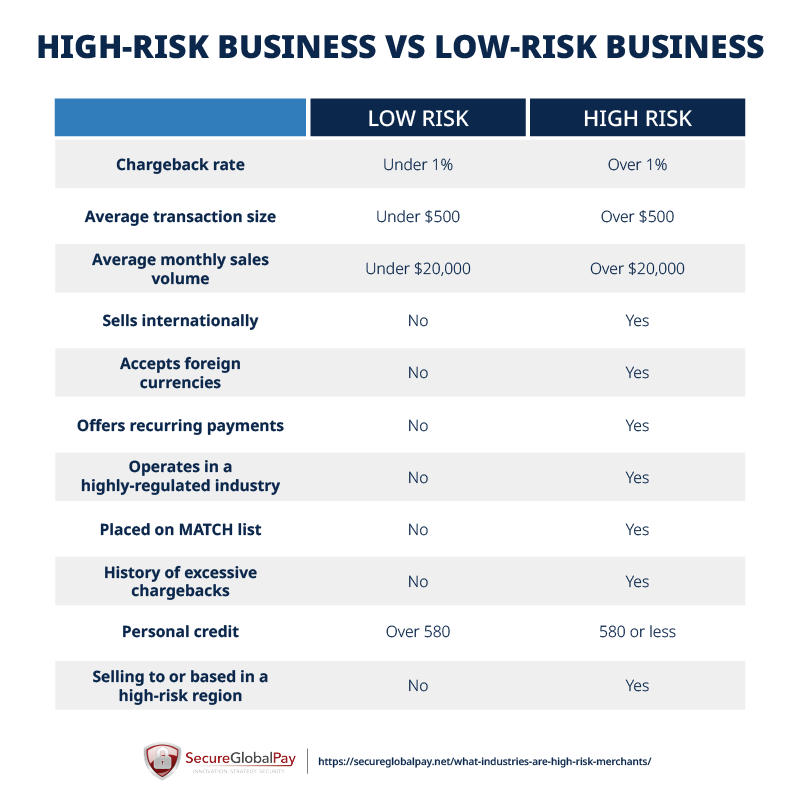

For reference, here is a quick table that shows which types of businesses are typically considered high-risk.

Now, if you are a high-risk business that wants to get a high-volume merchant account, you will have to jump through some hoops. It’s possible, but there might be additional requirements for high-volume credit card processing.

It is going to help if you’re selling goods or services that are not easily counterfeited or claimed as not having been provided. Great examples are doctors, lawyers, and online retailers.

Here are the key characteristics of a high-risk high-volume merchant account:

- Assessment of risk: High-risk businesses often include those in industries like travel, gaming, adult entertainment, or those with a history of chargebacks. The provider evaluates the risk associated with the volume and nature of transactions.

- Customized solutions: These accounts are tailored to handle the specific needs and risks of high-volume transactions. They might include features like advanced fraud detection, higher processing limits, and robust chargeback management.

- Higher fees: Due to the increased risk, high-risk high-volume merchant accounts typically come with higher processing fees and stricter terms.

- Enhanced security: Providers implement stringent security measures to protect against fraud, which is more prevalent in high-risk, high-volume environments.

- Regular monitoring: Continuous monitoring of transactions helps in the early detection of suspicious activities, reducing the risk of fraud and chargebacks.

- Increased reserves: Providers may require reserve amounts to safeguard against potential losses. This means a larger percentage of your sales is held back to cover any future chargebacks or disputes.

In summary, while not all high-volume merchant accounts are high-risk, many businesses with high transaction volumes will be treated as such. These accounts are designed to manage the increased risk and complexities.

Get high-volume credit card processing with SecureGlobalPay

We understand the unique challenges and needs that come with managing large transaction volumes. SecureGlobalPay’s mission is to provide tailored solutions that keep your operations running smoothly.

Why choose SecureGlobalPay?

- Competitive fees: We offer competitive transaction fees and various zero-fee processing programs you can utilize to keep more of your hard-earned revenue.

- High processing limits: Our accounts are designed to handle substantial transaction volumes so that you can scale your business without frequent requests for limit increases.

- Robust security: Our advanced fraud detection and prevention systems help protect your business and customers from fraudulent activities.

- Dedicated support: Our team of experts is available 24/7 to provide personalized support and quickly resolve any issues.

- Flexible contracts: We believe in transparency and flexibility, offering contract terms that suit your business needs without hidden fees or long-term commitments.

- Seamless integration: Our payment gateway can integrate with your existing software and e-commerce platforms, ensuring a smooth transition and ongoing operations.

- Reputation for excellence: We’ve been helping businesses across various industries accept and process payments for more than 20 years.

Getting started is easy. Fill out our merchant application form or reach out to partners@secureglobalpay.net with any questions you might have.

As your business grows, SecureGlobalPay is here to support you every step of the way. Our high-volume credit card processing solutions are designed to scale with your business, providing the reliability and efficiency you need to succeed.