Home » Best Fraud Prevention for High-Risk Merchants: Tips, Tools & Strategies

Best Fraud Prevention for High-Risk Merchants: Tips, Tools & Strategies

| April 15, 2026

Payment fraud is one of the most costly threats facing merchants today. Businesses lost more than $52 billion to online payment fraud in 2025 — and that number doesn’t account for the indirect costs of fighting it.

If you operate in a high-risk industry, the stakes are even higher. These sectors attract disproportionate fraud activity due to higher transaction volumes, digital delivery, and elevated chargeback rates.

Whether you’re building your payment fraud prevention stack from scratch or looking to strengthen what you already have, this guide will give you the knowledge and tools to do it right.

QUICK TAKEAWAYS

- Payment fraud costs merchants billions every year — and high-risk merchants face a disproportionate share of that exposure.

- Effective payment fraud management requires both prevention and detection working together.

- Your payment gateway is the foundation of your fraud stack; make sure it offers robust, built-in protections before adding third-party tools.

- Fraud prevention is not a one-time setup — continuously tuning your rules and adapting to changes in KPIs is what keeps your defenses effective over time.

- SecureGlobalPay offers a dedicated merchant account, a powerful payment gateway, dozens of integrations with different fraud and chargeback tools, and hands-on support for high-risk and e-commerce merchants.

Payment fraud management basics for high-risk merchants

Before you can build an effective defense, you need to understand what you’re up against. The most common types of fraud high-risk merchants face include:

- Card-not-present (CNP) fraud: A fraudster uses stolen card details to make purchases without physically presenting the card. CNP fraud is especially prevalent in e-commerce and digital transactions, where there’s no in-person verification.

- Identity theft: A bad actor steals someone’s personal information (name, address, Social Security number) and uses it to open accounts or make purchases. High-risk merchants are frequent targets because their products and services are easy to monetize.

- Friendly fraud (a.k.a chargeback fraud): A customer disputes a legitimate charge with their bank — sometimes out of buyer’s remorse, sometimes deliberately (to get their money back while keeping the goods or service). It accounts for a significant share of chargeback losses and is notoriously difficult to fight.

- Account takeover (ATO): A fraudster gains access to an existing customer account — often through phishing or credential stuffing — and uses it to make unauthorized purchases or drain stored value. ATO attacks are on the rise as more merchants store payment credentials for repeat customers.

When it comes to combating these threats, there are two main approaches: prevention and detection. The most resilient fraud programs use both in tandem.

| Aspect | Fraud prevention | Fraud detection |

| Timing | Before transaction | During or after the transaction |

| Purpose | Stop fraud from happening | Identify fraud quickly |

| Tools | Authentication, verification, rules | Monitoring, analytics, alerts |

| Outcome | Transaction blocked | Transaction flagged/investigated |

| Strength | Reduces fraud volume and exposure | Catches fraud that slips through prevention layers |

| Potential weakness | Adds friction (verification steps), false positives | Damage may already be done, requires investigation |

Payment fraud prevention (stopping it before it happens)

Payment fraud prevention refers to the tools, actions, and systems designed to block fraudulent transactions before they are completed. The goal is to avoid fraud entirely.

Prevention works by screening transactions and user behavior against known risk signals before authorizing a payment. Common prevention mechanisms include two-factor authentication (2FA), CVV and AVS checks, and biometrics.

Example: A customer attempts a purchase from an IP address in one country, but their billing address is in another, and the transaction amount is unusually high. The merchants’ fraud detection software flags the mismatch and declines the transaction before it goes through.

Payment fraud detection (catching it as or after it happens)

Payment fraud detection refers to the processes that identify suspicious or fraudulent activity during or after a transaction has occurred. The goal is to spot fraud quickly and respond before losses compound.

Detection relies on monitoring and pattern recognition to surface activity that deviates from the norm. Common detection techniques include behavioral analytics, anomaly detection, and alerts for suspicious transactions

Example: A cardholder’s account suddenly shows several high-value purchases at electronics retailers — a pattern that doesn’t match their usual spending. The fraud detection system flags the anomaly and sends an alert to the cardholder and the fraud team.

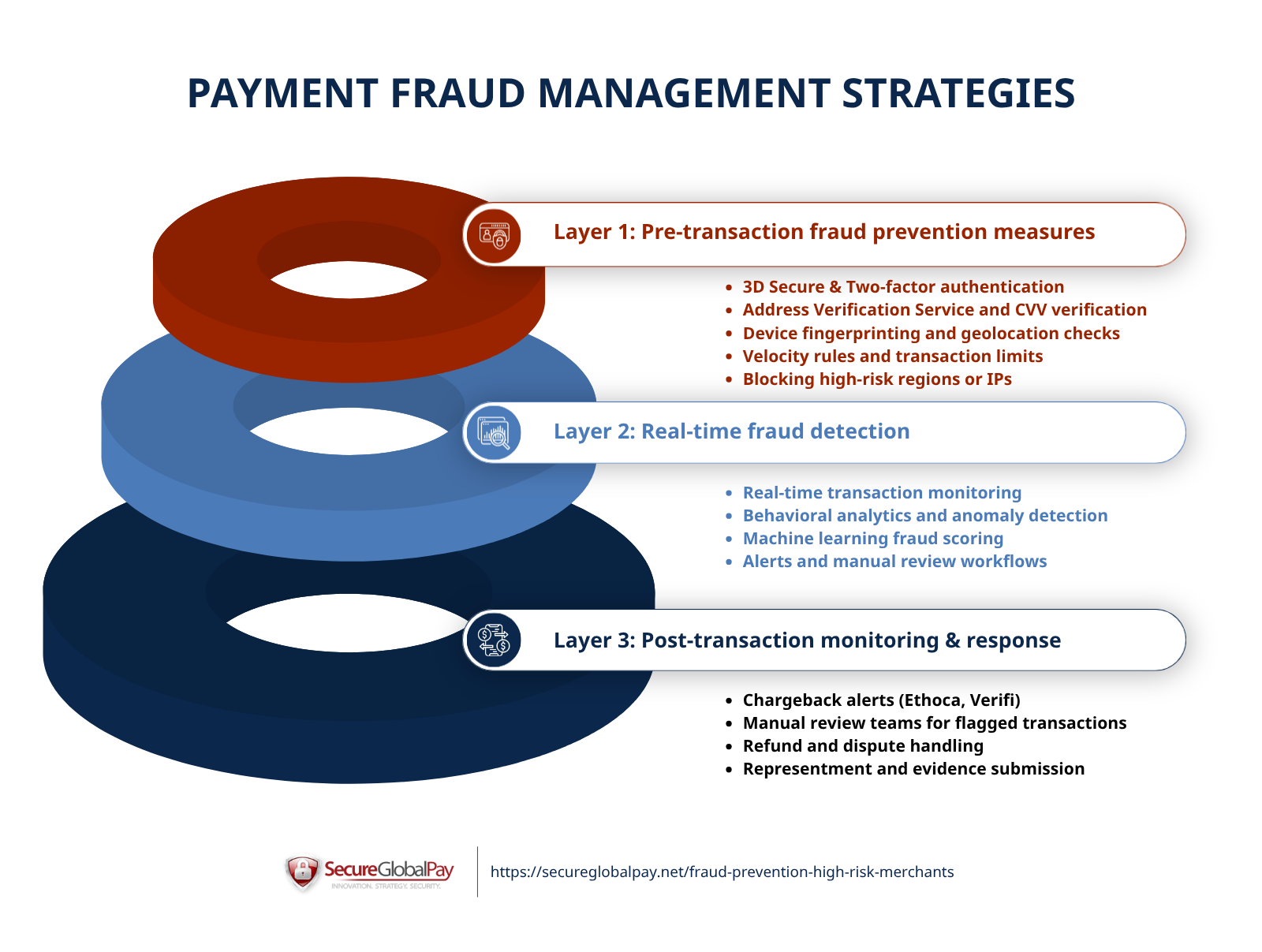

Fraud management strategies for high-risk merchants

The most effective fraud management programs don’t rely on a single tool or tactic. They use a layered approach, with controls operating at every stage of the transaction lifecycle: before, during, and after payment. Here’s how each layer works.

Layer 1: Pre-transaction fraud prevention measures

Pre-transaction fraud prevention is built on rule-based systems — sets of predefined conditions that automatically allow, flag, or block a transaction based on specific criteria.

For instance, a rule might block any transaction over $500 originating from a high-risk country, or flag any account that attempts more than three purchases in under two minutes. These rules execute instantly, requiring no human intervention.

Common pre-transaction prevention methods include:

- Identity verification and authentication: Tools like 3D Secure (3DS2) add an authentication step at checkout, prompting cardholders to verify their identity through their bank before a transaction is approved. Two-factor authentication (2FA) adds a second layer by requiring users to confirm their identity via a secondary channel — such as a one-time code sent to their phone.

- Card validation tools: AVS (Address Verification Service) checks whether the billing address entered at checkout matches what the card issuer has on file. CVV verification confirms the customer has the physical card in hand. Together, these checks weed out fraudsters using stolen card numbers alone.

- Device fingerprinting and geolocation checks: Device fingerprinting collects data points about the device being used — browser type, operating system, screen resolution, and more — to build a unique device profile. Geolocation checks cross-reference the transaction’s IP address with the cardholder’s billing address and prior activity to flag location mismatches.

- Velocity rules and transaction limits: Velocity rules monitor how frequently a card, account, or device is used within a set time window. A card that makes ten transactions in five minutes, for example, is almost certainly being tested by a fraudster — a tactic known as card testing.

- Blocking high-risk regions or IPs: Merchants can configure their fraud tools to automatically decline or flag transactions originating from IP addresses or regions associated with high fraud rates, known fraud networks, or jurisdictions where they don’t operate.

Dedicated pre-transaction fraud prevention platforms typically offer a combination of AI-driven risk scoring, real-time automated decisioning, behavioral data analysis, and identity verification across the customer journey. Leading vendors include Kount (now part of Equifax), Signifyd, Sift, and Forter.

Modern payment gateways include built-in pre-transaction controls — such as AVS matching, CVV verification, and basic velocity checks — as part of their standard offering. If you're a high-risk merchant, take time to understand exactly what your gateway covers before investing in additional tools.

Layer 2: Real-time fraud detection

While pre-transaction rules block many fraud attempts upfront, some slip through — especially sophisticated attacks that mimic legitimate behavior. Real-time fraud detection acts as your second line of defense, including techniques like:

- Real-time transaction monitoring: Every transaction is evaluated continuously against live data, allowing fraud teams and automated systems to intervene mid-stream if something looks off.

- Behavioral analytics and anomaly detection: Detection tools build a profile of normal behavior for each customer — typical spend amounts, purchase frequency, device usage, and more. Deviations from that profile, such as a sudden spike in transaction value or purchases from an unfamiliar device, trigger an alert or automatic action.

- Machine learning fraud scoring: Machine learning models analyze hundreds of data points per transaction and assign a fraud risk score in milliseconds. Transactions that exceed a set risk threshold are automatically flagged for review or declined.

- Alerts and manual review workflows: When automated systems flag a transaction, they route it to a review queue or send an alert to the fraud team. Well-designed workflows ensure that high-risk transactions get human eyes quickly, without creating bottlenecks for legitimate orders.

Dedicated real-time fraud detection platforms typically offer machine learning-based risk scoring, behavioral analytics, customizable alert thresholds, and case management tools for manual review teams. Popular platforms include Stripe Radar, Accertify, Featurespace, and DataVisor.

Layer 3: Post-transaction monitoring & response

Even with strong prevention and detection in place, some fraud still gets through — and chargebacks are often the result.

Post-transaction monitoring and response focus on identifying fraud after it has occurred, managing disputes, and recovering lost revenue. For high-risk merchants, this layer is especially critical: chargeback ratios above card network thresholds (think VISA VAMP) can put your merchant account at risk.

Common post-transaction methods include:

- Chargeback alerts: Services like Ethoca and Verifi notify merchants of a dispute the moment it is filed, giving you a short window to issue a proactive refund and prevent the chargeback from being recorded against your account.

- Manual review teams: Dedicated fraud analysts review flagged transactions, disputed orders, and patterns in chargeback data to identify root causes and catch fraud that automated systems missed.

- Refund and dispute handling: When a chargeback cannot be prevented, merchants can fight it through the representment process — submitting evidence to the card network to prove the transaction was legitimate. Well-organized evidence, submitted on time, is essential to winning disputes.

Top vendors include Chargebacks911, Verifi (backed by Visa), Chargeflow, and Justt. Many of these platforms come with chargeback alert integrations, automated evidence collection and submission, dispute tracking dashboards, and tools that simplify root-cause analysis.

Best practices for preventing and catching payment fraud

How you configure, combine, and maintain your fraud management program is almost as important as which tools you use. These best practices will help you get the most out of your fraud stack and stay ahead of evolving threats.

Process transactions through a secure payment gateway

Your payment gateway is the foundation. Every transaction flows through it, which means the protections built into your gateway are your first and most consistent line of defense. For high-risk merchants especially, choosing a gateway with robust security is non-negotiable.

A powerful payment gateway should offer the following protections out of the box: PCI DSS compliance, SSL/TLS encryption, tokenization, AVS and CVV verification, 3DS support, velocity controls, transaction limits, real-time monitoring and alerts, and native integrations with popular 3rd-party chargeback and fraud management tools

A strong gateway reduces how much you need to rely on external tools to fill security gaps.

Leverage fraud protection tools

Even with a powerful payment gateway, most high-risk merchants should also consider a dedicated fraud protection tool. You can choose between:

- End-to-end fraud platforms: Tools like Kount and Sift cover the full spectrum, from pre-transaction risk scoring to post-transaction analysis, in a single platform.

- Prevention-focused tools: Solutions like Forter and Signifyd specialize in stopping fraud before a transaction is approved, using identity intelligence and automated decisioning.

- Detection-focused tools: Platforms like Featurespace and DataVisor focus on real-time anomaly detection and behavioral analytics to catch fraud as it happens.

- Chargeback management tools: Services like Chargebacks911, Chargeflow, and Justt focus specifically on dispute prevention, evidence management, and chargeback representment.

The right starting point is to audit what your gateway already covers, then identify the gaps. From there, your choice of additional tools should be guided by a few key factors:

- Budget: Entry-level tools like Stripe Radar are cost-effective for lower-volume merchants, while enterprise platforms like Forter or Kount are better suited to merchants with higher transaction volumes and the budget to match.

- Industry risk level: The higher your fraud exposure, the more layers you need. A nutraceuticals merchant processing hundreds of card-not-present transactions per day has different needs than a low-volume B2B seller.

- Transaction volume: High-volume merchants benefit most from fully automated, machine learning-driven platforms.

Some larger merchants opt to build custom fraud models in-house, which offers maximum flexibility but requires significant technical resources. For most high-risk merchants, buying or subscribing to an established platform is faster, more cost-effective, and easier to maintain.

Combine automation with manual review

A well-designed fraud program uses automation to handle the clear-cut cases — approving low-risk transactions and blocking obvious fraud — while routing ambiguous cases to a human reviewer.

A few tips for combining automation and manual review effectively:

- Set clear thresholds: Define which risk scores or rule triggers automatically approve, automatically decline, and escalate to manual review.

- Prioritize your review queue: Not all flagged transactions are equal. Sort manual review cases by transaction value, risk score, or customer history so your team tackles the highest-stakes decisions first.

- Document reviewer decisions: When a reviewer approves or declines a flagged transaction, log the reasoning. This data is invaluable for tuning rules over time.

- Staff appropriately for volume spikes: Fraud attempts tend to spike during high-traffic periods like holidays or major sales events. Make sure your manual review capacity scales with your transaction volume during these windows.

Continuously tune rules and models

If you set up your fraud tools and never revisit them, you’re essentially fighting new threats with old defenses.

Tuning should be done regularly — not just after a spike in fraud or chargebacks. Review your rules and model performance at least monthly, looking for patterns in false positives, false negatives, and chargeback root causes.

When new fraud patterns emerge, update your rules promptly. If transactions approved by reviewers frequently result in chargebacks, your thresholds are too lenient. When a rule consistently blocks legitimate customers without catching fraud, retire or adjust it.

Segment customers by risk

Risk-based segmentation tailors your fraud controls to the actual risk profile of each customer or transaction.

In practice, this means grouping customers into risk tiers based on signals like purchase history, account age, device reputation, location, and payment method.

Returning customers with a clean history can be fast-tracked with minimal friction, while new accounts, unusual order patterns, or mismatched data points trigger additional scrutiny.

Most modern fraud platforms support dynamic risk segmentation out of the box — but you need to define the criteria that make sense for your business, your customer base, and your industry risk level.

Monitor relevant KPIs

Without tracking the right metrics, you won’t know whether your controls are working as intended. A few useful metrics to track include:

- Chargeback rate: The percentage of transactions that result in a chargeback. If this is trending upward, your prevention and detection layers need attention. Card networks typically flag merchants who exceed 1% (Visa) or 1.5% (Mastercard).

- False positive rate: The percentage of legitimate transactions your system incorrectly blocks. A high false positive rate means lost revenue and frustrated customers — it’s just as damaging as fraud itself.

- Fraud-to-sales ratio: The percentage of total revenue lost to fraud. This gives you a high-level view of your overall fraud exposure and how it changes over time.

- Manual review queue size: If your queue is consistently large, your automated thresholds probably need adjustment. A bloated review queue slows decisions and increases the risk of missing deadlines.

- Chargeback dispute win rate: The percentage of disputed chargebacks you successfully win through representment. A low win rate signals a need to improve your evidence collection and submission process.

Use the trends you see to drive concrete changes — tightening rules when fraud spikes, loosening thresholds when false positives climb, and escalating to your fraud tools provider when something falls outside your ability to address internally.

Don’t repeat the same mistakes

It’s nearly impossible to configure everything perfectly the first time around. Here are the three most common mistakes high-risk merchants make:

- Over-blocking customers: Setting fraud rules too aggressively leads to high false positive rates, frustrated legitimate customers, and lost revenue. Regularly audit your declined transactions to make sure you’re not turning away good business.

- Relying on only one tool: With maybe a few exceptions, no single platform covers every threat. A payment gateway with basic fraud controls, a fraud prevention platform, and a chargeback management tool serve different purposes — and hard-to-place merchants need all three layers working together.

- Not adapting to new fraud patterns: Fraudsters continuously refine their tactics. Static rules and untuned models become less effective over time. If you’re not actively updating your fraud program, you’re building up unnecessary risk.

Best fraud prevention measures for high-risk e-commerce

High-risk e-commerce merchants face a particularly aggressive fraud environment. The combination of card-not-present transactions, digital product delivery, and high order volumes creates ideal conditions for fraudsters.

According to Juniper research, the value of eCommerce fraud will rise from $44.3 billion in 2024 to $107 billion in 2029. The most damaging threats are CNP fraud and friendly fraud. Both are difficult to detect in the moment and costly to fight after the fact.

When setting up a high-risk e-commerce merchant account, consider the following measures:

- Use a high-risk payment gateway: Not all gateways are built to handle the elevated chargeback ratios and scrutiny that come with high-risk industries. Work with a gateway specifically designed for high-risk merchants, with built-in fraud controls and proper integrations.

- Enable 3D Secure 2 (3DS2): 3DS2 adds an issuer-verified authentication step at checkout, shifting liability for fraudulent chargebacks from you to the card issuer on authenticated transactions.

- Require CVV and AVS on every transaction: Never process a card-not-present transaction without validating both the card verification value and the billing address.

- Implement device fingerprinting: Identify and track the devices used to place orders. Flagging known fraudulent devices or unusual device-location combinations stops repeat offenders before they can strike again.

- Set velocity rules for card testing: Card testing is rampant in e-commerce. Velocity rules that limit the number of transactions per card, device, or IP address within a set time window are an effective countermeasure.

- Use fraud scoring on every order: Integrate a fraud scoring tool that evaluates every transaction in real time before fulfillment, especially for digital goods that are delivered instantly and are impossible to recover once sent.

- Monitor for friendly fraud patterns: Track customers who repeatedly dispute transactions or request refunds. Flagging these accounts for additional scrutiny on future orders reduces your exposure to repeat friendly fraud.

- Integrate chargeback alert services: Services like Ethoca and Verifi notify you the moment a dispute is filed, giving you a window to resolve it before it becomes a recorded chargeback against your account.

- Keep detailed transaction records: Maintain comprehensive records for every transaction — IP address, device data, order details, delivery confirmation, and customer communication. Strong documentation is your best weapon in a chargeback dispute.

How SecureGlobalPay protects high-risk merchants from chargebacks and fraud

SecureGlobalPay is an all-in-one merchant services provider built specifically for high-risk businesses.

We offer everything you need to accept payments confidently: a dedicated merchant account, a powerful payment gateway with all of the bells and whistles, dozens of integrations with different fraud and chargeback tools, and hands-on support from industry veterans that will help you avoid common mistakes and configure your tools properly.

Don’t waste time opening an account at Stripe or PayPal. If you are a high-risk merchant, sign up with SecureGlobalPay and enjoy all of the protections that come from our dedicated payment gateway.

FAQs

The best fraud tools for high-risk merchants span several categories: identity verification (Persona, Jumio), fraud prevention and scoring (Kount, Forter, Signifyd, Sift), real-time transaction monitoring (Featurespace, DataVisor), chargeback alerts (Verifi, Ethoca), and chargeback management (Chargebacks911, Chargeflow, Justt). Most high-risk merchants benefit from combining tools across at least two or three of these categories rather than relying on a single platform.

Merchant risk is typically assessed across four dimensions:

- Industry risk: Some industries (e.g., gambling, nutraceuticals, adult content, firearms, travel) are inherently considered high-risk by banks and card networks due to regulatory exposure, chargeback rates, or reputational factors

- Financial risk: Elevated chargeback ratios, high refund rates, or a history of fraud losses signal financial instability to acquiring banks

- Reputational risk: Association with controversial, heavily regulated, or legally complex products or services that could expose a payment processor to liability

- Operational risk: Factors like limited processing history, poor compliance practices, high transaction volumes, or irregular business models that increase the likelihood of financial loss for the acquiring bank

3D Secure reduces fraud-related chargebacks by shifting liability from the merchant to the card issuer on successfully authenticated transactions. However, it does not cover non-fraud chargebacks — such as friendly fraud or “item not received” disputes. For full chargeback protection, 3DS should be combined with additional fraud controls and a dedicated chargeback management tool.

Written By

R

Roland G. Szasz

Director of Business Development at SecureGlobalPay

Roland has spent nearly three decades helping businesses navigate the complexities of payment processing. He now works closely with high-risk merchants that have been declined or restricted by conventional providers - and shares his experience and best practices on this blog.

Tailored payment solutions for high-risk merchants

- Domestic and offshore accounts

- Competitive, interchange plus pricing

- No long-term contracts or hidden fees

- Built in fraud protection

- Dedicated account manager; 24/7

Sign up in 5 minutes

A+ Rating

as of 06/17/26

Related Posts