Home » Merchant Accounts Explained – Types and How They Work

Merchant Accounts Explained – Types and How They Work

| December 29, 2024

A merchant account is essential for businesses that want to accept payments via credit cards, debit cards, and other electronic payment methods.

Understanding how merchant accounts work is key to choosing the right provider for your business. Whether you’re running a retail store, an online shop, or a high-risk business, having the proper merchant account setup makes all the difference.

QUICK ONLINE APPLICATION

Complete payment processing solutions for both retail and high-risk merchants.

In this article, we’ll break down everything you need to know about merchant accounts: what they are, how they work, the different types of merchant accounts available, and how to open one.

QUICK TAKEWAYS

- A merchant account enables businesses to securely process payments and transfer funds to their bank accounts.

- Common types of merchant accounts include retail and high-risk, as well as aggregator solutions like PayPal or Stripe.

- High-risk merchant accounts face higher fees and stricter requirements but gain specialized fraud protection and chargeback tools.

What is a merchant account?

A merchant account acts as an intermediary between your customer’s bank account and your business bank account, facilitating a secure and efficient transfer of funds.

While a regular bank account is used to store and manage your business funds, a merchant account is specifically designed to process payments. It temporarily holds the funds from customer transactions until they are cleared and transferred to your business bank account. This process ensures secure payment verification and helps prevent fraud.

Who needs a merchant account? Retail stores, eCommerce businesses, restaurants, service providers, high-risk merchants — any business that wants to accept in-person card payments or online payments.

Merchant accounts are provided by:

- Acquiring banks: Financial institutions that hold the merchant account and process payments on behalf of the business.

- Payment processors: Companies that handle the technical aspects of payment transactions, such as verifying card details and transferring funds. These providers also offer additional tools like fraud protection, analytics, and integration with point-of-sale (POS) systems.

How do merchant accounts work?

Here’s a step-by-step example of how a merchant account works during a typical credit card transaction:

- Customer initiates payment: A customer purchases a product or service and provides their payment details, either by swiping a credit card, entering information online, or using a mobile wallet.

- Payment processor verifies details: The payment information is sent to the payment processor, which communicates with the customer’s issuing bank to verify the card details and confirm there are sufficient funds.

- Transaction approved: If the details are correct and funds are available, the transaction is approved.

- Funds transferred to merchant account: The approved transaction triggers the transfer of funds to the merchant account, where they are temporarily held.

- Settlement to business bank account: After processing fees are deducted, the funds are transferred from the merchant account to the business’s bank account, typically within 1-3 business days.

This process happens almost instantaneously for the customer, but the backend involves multiple steps to ensure security and accuracy.

Common types of merchant accounts

When it comes to merchant accounts, there is no one-size-fits-all solution. Different types of businesses require different types of merchant accounts, depending on factors like risk level, transaction volume, and how payments are processed.

In this section, we’ll explore the most common types — and which businesses they are best suited for.

Retail merchant accounts

Retail merchant accounts are designed for businesses that primarily accept in-person payments. These accounts are used by brick-and-mortar stores where customers pay using physical credit or debit cards through a point-of-sale (POS) terminal.

In other words, retail merchant accounts are perfect for businesses that handle a high volume of face-to-face transactions like:

- Retail stores

- Restaurants

- Service-based businesses with physical locations, such as salons or gyms.

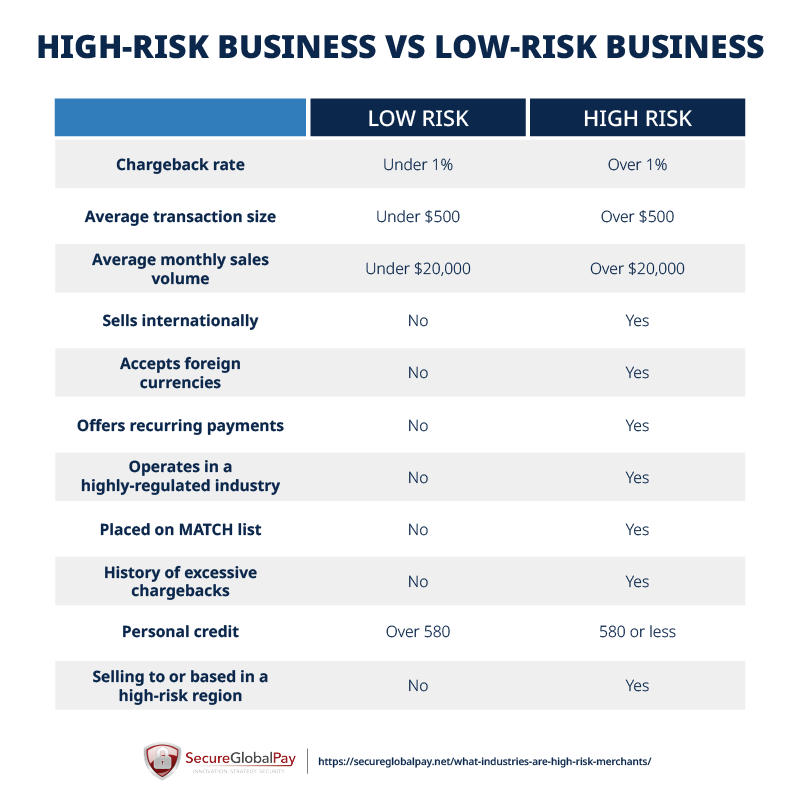

High-risk merchant accounts

High-risk merchant accounts are specifically designed for businesses that operate in industries with a higher risk of fraud, chargebacks, or regulatory scrutiny. Banks and payment processors categorize these businesses as high-risk because of the potential financial exposure involved.

Contrary to popular belief, the high-risk label is not reserved for shady industries. It actually covers a vast number of different industries and business models, including:

- Online gaming and gambling

- Adult entertainment

- Firearm sales

- Subscription-based businesses

- Travel and ticketing services

- Businesses selling high-ticket items or pushing high-transaction volumes

- Other businesses with a history of high chargebacks or financial instability.

High-risk merchant accounts come with higher processing fees and additional requirements, such as the need to have reserve accounts. On the flip side, you also get access to specialized fraud detection tools and chargeback management systems.

Merchant aggregators

Merchant aggregators, also known as payment aggregators, allow businesses to accept payments without needing to set up their own individual merchant account. Instead, businesses are grouped under a single master merchant account provided by the aggregator.

Square, PayPal, and Stripe are some of the most popular aggregators on the market. They can be a good fit for:

- Small businesses

- Freelancers and independent contractors

- Businesses with low transaction volumes

- Startups that need a simple payment solution

These services make it easy for businesses to start accepting payments quickly, but they are generally not a great long-term solution.

Other types of merchant accounts

Merchant accounts can also be categorized based on how payments are accepted and the nature of the business:

- Online/Internet/E-commerce merchant accounts: Designed for businesses that primarily accept payments online through websites or mobile apps.

- Mobile merchant accounts: Ideal for businesses that accept payments on the go, using mobile devices and card readers.

- MOTO (Mail Order/Telephone Order) merchant accounts: Used by merchants that process payments remotely, via mail or phone.

- Offshore merchant accounts: Useful for businesses operating in international markets or industries where domestic merchant accounts might not be available.

Free e-Book: Credit Card Processing 101

Get our free Credit Card Processing 101 guide and finally make sense of pricing models, payment systems, and costs involved — so you can keep more of what you earn.

The process for opening a merchant account

Opening a standard merchant account is fairly simple. All you need to do is:

- Select a payment provider: Research and choose a payment processor or acquiring bank that fits your business needs, considering factors like fees, support, and features.

- Submit an application: Provide the necessary details, including business information, financial history, and documentation such as identification, business licenses, and bank statements.

- Wait for approval: The payment provider will review your application to assess risk and determine eligibility. This process may involve credit checks and evaluation of your business model.

- Set up your merchant account: Once approved, the provider sets up your merchant account (e.g. set up the POS system and/or implement payment processing on your website by integrating it with a payment gateway).

If you are a high-risk merchant, the process is basically the same. However, you will need to provide more information when you apply for a merchant account, and there is a higher likelihood of your application being rejected.

Get a (high-risk) merchant account at SecureGlobalPay

At SecureGlobalPay, we specialize in providing reliable merchant account solutions for businesses of all types, including those categorized as high-risk.

Here is what you get:

- Competitive rates: We offer transparent and competitive pricing with no early cancellation or other hidden fees.

- Fast and secure processing: With SecureGlobalPay, you can start accepting payments quickly while ensuring secure transactions for your customers.

- Omnichannel payments: Accept credit/debit cards and MOTO transactions, Google and Apple Pay, online, retail, self-service, and mobile payments — including EMV, contactless, ACH, and eCheck payments.

- Tailored high-risk solutions: We work with businesses in industries like subscription services, adult entertainment, and travel to provide customized merchant accounts that meet their needs.

- Advanced fraud protection: SecureGlobalPay provides cutting-edge tools to help reduce fraud and manage chargebacks effectively.

- A huge number of integrations: Our modern payment gateway can connect to most major eCommerce platforms and shopping carts.

- Global reach: We support businesses that need offshore merchant accounts or operate internationally, ensuring seamless payment processing across borders.

- Amazing support team: Our dedicated account managers have 10+ years of industry experience and can help you solve almost any issue.

Contact us today to discuss your needs and get your business set up with a secure, flexible, and reliable merchant processing solution.

Merchant Account FAQ

A local coffee shop might set up a merchant account with a payment processor like SecureGlobalPay. When a customer pays with a credit card, the transaction is processed through the merchant account, and the funds are then transferred to the coffee shop’s business bank account after fees are deducted.

No, PayPal itself is not a traditional merchant account. Instead, it functions as a payment aggregator. This means that PayPal groups multiple businesses under a single master merchant account, which PayPal owns.

When you use PayPal to accept payments, you don’t have to open a dedicated merchant account of your own. Instead, PayPal processes transactions on your behalf and temporarily holds the funds in your PayPal account. From there, you can transfer the funds to your bank account or use them directly through PayPal.

The time it takes to get approved for a merchant account can vary depending on the provider and the nature of your business. On average, approvals take 1-3 days for low-risk businesses and 3-7 days for those categorized as high-risk.

Payment aggregators often allow businesses to start accepting payments almost immediately, as there’s minimal underwriting. However, they may place restrictions on transactions until additional verification is completed.

Yes, you can still open a merchant account even if you have bad credit, but the process may be more challenging. Traditional banks and payment processors might decline your application, but there are specialized providers like SecureGlobalPay that focus on high-risk and bad-credit businesses.

The only way to accept payments online without a traditional merchant account is by using payment aggregators like PayPal, Stripe, or Square. However, a dedicated merchant account is a better long-term solution for businesses with higher transaction volumes or specific processing needs.

Posted in - Merchant Accounts, Payment Aggregators

Start Accepting

Payments Today

Payments Today