Home » What is Intelligent Payment Routing? Tools & Best Practices

What is Intelligent Payment Routing? Tools & Best Practices

| May 13, 2026

Many merchants still use static payment setups in which every transaction follows the same route, no matter where the customer is located or which card they use.

That approach is simple to set up, but it often leaves money on the table through avoidable declines, higher fees, and lost sales during outages or slowdowns.

Smart payment routing changes that. Instead of sending every payment down one fixed lane, intelligent routing helps merchants choose the best path in real time based on factors like customer geography, transaction risk, costs, and failover availability.

For businesses processing high volumes, selling internationally, or operating in higher-risk industries, this can make a major difference in approval rates and payment resilience.

In this guide, we’ll explain what intelligent payment routing is, how it works, why it matters, and how merchants can use it to build a stronger, more profitable payment technology stack.

QUICK TAKEAWAYS

- Smart routing uses live data such as geography, provider performance, and transaction type to optimize the path of each transaction.

- Businesses that sell globally, process high volume, or operate in higher-risk industries can gain the most from intelligent routing strategies.

- SecureGlobalPay provides a smart routing payment gateway designed to help merchants scale, improve approvals, and support global high-risk payment needs.

What is smart payment routing?

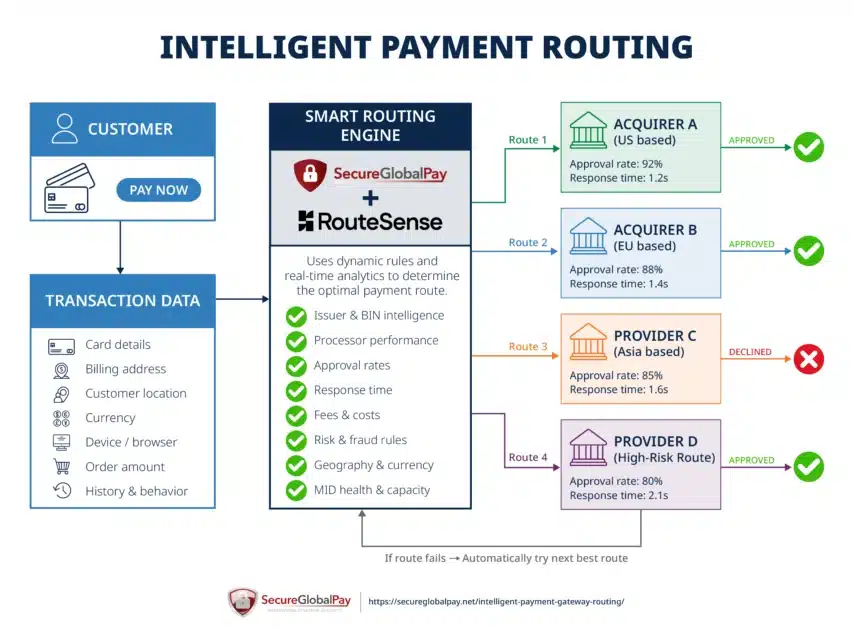

Smart payment routing (also called intelligent payment routing) is the process of sending each transaction through the payment path most likely to deliver the best outcome.

The system (your payment gateway or payment orchestration platform) evaluates relevant factors in real time — such as customer location, card issuer, currency, processor performance, fees, risk signals, or provider availability — and chooses the most suitable route.

That route might be:

- Sending a European customer’s payment to a local acquirer.

- Directing a recurring subscription charge to a processor with strong rebilling.

- Distributing transactions across multiple accounts and providers during sales spikes to remain under approved thresholds on all accounts.

- Forwarding a sale of a high-risk product to a dedicated merchant account.

- Switching traffic to a backup provider if the primary one is slow or unavailable.

Traditional payment routing works very differently. In many older setups, every transaction is sent to the same acquiring bank or follows a fixed set of manual rules. While this can be easier to manage at first, it often leads to lower approval rates and avoidable costs.

| Traditional Payment Routing | Intelligent Payment Routing |

| Uses one main processor or fixed routes | Can use multiple routes and acquiring banks; chooses the best option dynamically |

| Same path for most transactions | Different paths based on transaction data, costs, and likelihood of approval |

| Manual changes required | Automated real-time decision making |

| Limited failover options | Built-in backup routing and redundancy |

| Harder to optimize international payments | Supports local and cross-border optimization |

| Fees may remain unnecessarily high | Can route based on cost efficiency |

| Slower to react to outages or declines | Adjusts quickly to downtime or approval issues |

| Better for simple setups | Better for scaling, global, or high-volume businesses |

In other words, smart routing gives merchants more control and better performance.

How does smart payment routing work?

Smart payment routing usually happens inside the payment gateway or orchestration layer. When a customer submits a payment, the system reviews key transaction details in real time and decides which processor, acquirer, or merchant account is the best route for that specific payment.

Common factors used in routing decisions include:

- Customer country or region

- Card issuer location

- Currency used at checkout

- Card brand or BIN range

- Transaction amount

- Cost per route

- Product type or risk level

- Historical approval rates

- Payment type (subscription vs one-time payment)

- Current processor uptime and response speed.

Once the best route is selected, the transaction is sent to that provider for authorization. If the route fails due to a timeout, technical error, or temporary decline, the system may automatically retry through another available provider.

Quick example: A customer in Germany places an order on a global e-commerce site using a Visa card. Instead of sending the payment to the merchant’s default US processor, the gateway recognizes that a European route may perform better. It sends the transaction through a European acquirer that supports local processing in euros.

Routing decisions can be rule-based (manually created logic; “UK cards go to UK acquirer”), dynamic (updated in real time based on various factors), or hybrid (fixed business rules combined with live performance data). The strongest setups use historical approval trends, current system conditions, and transaction context to choose the best route at the exact moment of payment.

The importance of intelligent payment routing for high-risk and high-volume merchants

If you process large volumes, sell across multiple countries, operate in a high-risk industry, or depend heavily on card payments, even small improvements in approvals or uptime can have a major revenue impact.

High-risk and high-volume merchants often face more declines, stricter provider rules, higher fees, and greater exposure to downtime. To a lesser or greater degree, smart routing helps reduce all of these risks.

Here are common situations in which your business may benefit from intelligent payment routing:

- You sell internationally: Different regions often perform better with local acquiring, local currencies, and region-specific payment routes.

- You process a large monthly volume: At scale, a small increase in approvals or lower costs can create meaningful gains. Plus, being able to route transactions to other MIDs helps you stay under your approved processing volume (this is called load balancing).

- You experience unexplained declines: Some declines are caused by issuer preferences, routing mismatches, or processor limitations — not the customer’s card.

- Payment fees are rising: Different providers may offer better rates depending on geography, volume, or payment type.

- You need backup acquiring options: Extra acquiring relationships create flexibility if one provider tightens underwriting or changes policies, especially with the latest VISA VAMP changes.

- You process high-ticket items: Larger transactions often need stronger approval strategies and more specialized acquiring options. Smart routing gives you the needed flexibility.

- You’re entering new markets: Selling in new countries may require an offshore merchant account and local processing relationships for better acceptance rates.

- You want to balance fraud protection and conversion rate: Smart routing allows merchants to send higher-risk transactions through routes with stronger fraud screening while keeping lower-risk payments on faster, lower-friction paths.

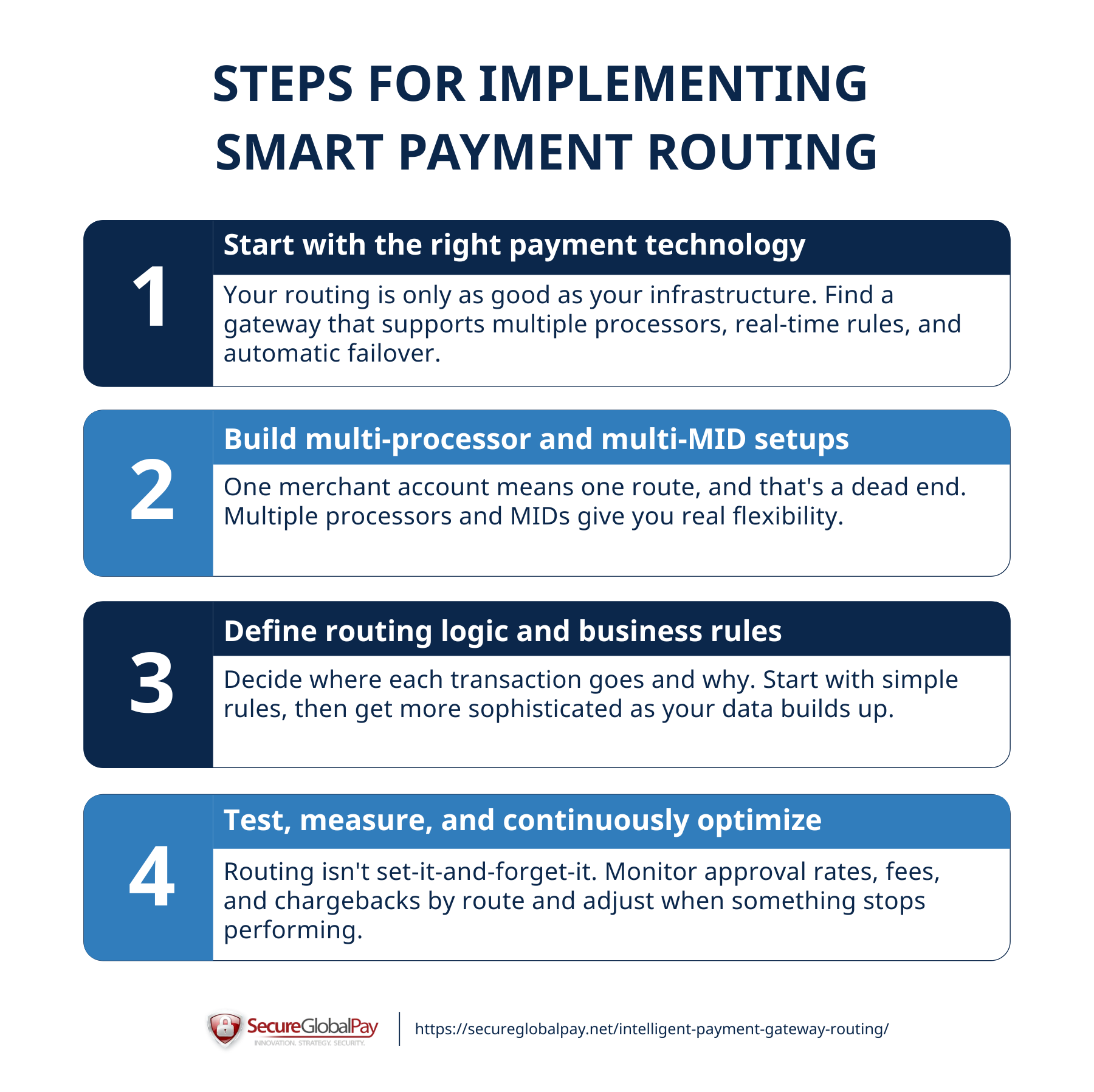

Steps for implementing intelligent payment routing

While payment routing might seem daunting for the non-initiated, know that the technology that runs in the background will do most of the heavy lifting.

Many businesses start with a simple multi-MID or multi-processor setup and improve their routing strategy over time as volume grows, new markets are added, or payment needs become more complex.

1. Start with the right payment technology

Smart routing depends on a payment infrastructure that can support multiple accounts, processors, acquirers, and routing logic without creating unnecessary operational complexity. Many older gateways only support basic static routing, which limits flexibility and makes optimization harder.

Merchants should look for a modern payment gateway or orchestration platform that can support:

- Multiple accounts, processors, and acquirer connections

- Real-time routing rules

- Automatic failover capabilities (instantly switching a transaction to a backup processor or merchant account when the primary route fails or performs poorly)

- Unified reporting across providers and merchant accounts

- Tokenization and vault portability

- Wide range of currencies and payment methods

- API flexibility for future expansion

- Easy integrations with merchant account health monitoring tools, CRMs, ecommerce platforms, checkout, billing, and other business systems.

The goal is to choose technology that can grow with the business and avoid costly custom integrations and configurations.

2. Build multi-processor and multi-MID setups

If every payment has to go through a single merchant account, your routing options are limited from the start.

That is why many growing businesses build multi-processor and multi-MID setups. This may include adding multiple processors, acquiring banks, or Merchant Identification Numbers (MIDs) across regions, brands, products, or risk profiles.

This way, you gain the flexibility to route transactions based on all the factors we talked about earlier. More routes create more opportunities to improve approvals, lower costs, and protect revenue.

3. Define routing logic and business rules

Once multiple routes are available, merchants need clear logic that decides where each transaction should go.

Here are a few examples of simple payment routing rules you can set up in your payment gateway:

- UK cards → UK acquirer

- Large-ticket orders → processor with the strongest approval history

- Subscription renewals → route optimized for recurring billing

- High-risk product orders → dedicated MID with suitable risk settings

- Traffic automatically shifted if a provider slows down or is unavailable.

Most businesses begin with simple rules, then make them more complex or dynamic over time as more performance data becomes available.

Using our gateway, you can create two separate lists of rules: one for credit cards and another one for eChecks.

Below is an example of transaction routing from our payment gateway tutorial series. It’s very simplistic and focused on load balancing, but it should give you an idea of what setting rules looks like in practice.

4. Test, measure, and continuously optimize

Intelligent payment gateway routing is not a one-time setup. Issuer behavior, processor performance, fraud patterns, and processing costs can change regularly. A route that performs well today may underperform next month.

Key metrics to monitor include:

- Overall authorization rate

- Approval performance by country, region, and provider

- Approval rate for local acquiring vs offshore acquiring

- Soft & hard decline rates

- Checkout abandonment after decline

- Total fees by processor or acquirer

- Cost per successful transaction by route or MID

- Chargeback trends by route or MID.

High-volume businesses should regularly test changes, measure results, and refine their routing logic based on real performance data — shifting volume to stronger providers, retrying soft declines through secondary route, removing weak routes, lowering costs, and improving approvals.

In time, this turns your payment data into a real competitive advantage.

Why you should use SecureGlobalPay’s smart routing payment gateway

Choosing the right gateway is what makes intelligent payment routing practical. You need a solution that can work with multiple MIDs, automate routing decisions, and give you clear visibility into performance — all without creating unnecessary complexity.

SecureGlobalPay is an all-in-one merchant services provider focused on high-risk, high-volume, and international merchants. Our payment gateway is built to help merchants improve approvals, scale globally, and create more resilient payment operations.

Key features include:

- Domestic and offshore merchant accounts

- Intelligent payment gateway routing based on performance and business rules

- Multi-MID and multi-processor support

- Built-in backup routing and failover tools

- AI-powered fraud protection

- Global payment support with numerous currencies and conversion options

- Over 200 native integrations with ecommerce platforms, chargeback tools, billing & invoicing software, and other business platforms

- RouteSense integration

- Centralized reporting across payment routes

- Dedicated setup and ongoing customer support.

If you want a smarter payment setup, sign up with SecureGlobalPay or schedule an exploratory call and see how intelligent routing can help your business grow.

FAQs

Smart routing is one feature within a broader payment orchestration strategy. Smart routing focuses specifically on deciding the best processor, acquirer, or payment path for each transaction, while payment orchestration manages the full payment ecosystem, including multiple providers, tokenization, retries, reporting, fraud tools, and payment method connections.

In simple terms, orchestration is the overall control layer, and smart routing is one of the key optimization tools inside it.

In most cases, yes. A modern payment gateway or payment orchestration platform is usually the easiest and most practical way to implement intelligent routing because it connects multiple processors and applies routing logic in real time.

Geographic routing uses customer location, issuer country, currency, or regional payment behavior to decide where a transaction should be processed. For example, a European customer may be routed to a European acquirer, while a US customer is sent to a domestic provider. This often improves approval rates, reduces cross-border fees, speeds up authorization, and creates a smoother local checkout experience.

International routing works by matching each transaction to the most effective payment route based on country, currency, card issuer, and provider performance in that region. A gateway may send transactions through local acquirers, support local currencies, or choose providers with stronger regional approval history.

The most common challenges include connecting multiple processors and MIDs, creating effective routing rules, consolidating reporting, and maintaining compliance across markets. Businesses may also struggle with added operational complexity if the system is not managed through a strong gateway or orchestration layer.

Common mistakes include using static routing for all transactions, failing to monitor approval performance, ignoring regional differences, optimizing only for fees, and not setting up backup routes.

Yes, but it usually requires significant technical resources, processor integrations, compliance oversight, monitoring systems, and ongoing maintenance. Large enterprises sometimes build custom routing engines for maximum control, but many merchants find it faster and more cost-effective to use an existing gateway or orchestration platform with built-in smart routing features.

Yes. SecureGlobalPay provides a payment gateway designed to support intelligent routing, multi-MID setups, backup processing paths, fraud protection, and global payment acceptance. It is built to help merchants improve approval rates, strengthen resilience, and manage more complex payment operations.

Posted in - High-Risk Payment Processing, Payment Gateways

Written By

R

Roland G. Szasz

Director of Business Development at SecureGlobalPay

Roland has spent nearly three decades helping businesses navigate the complexities of payment processing. He now works closely with high-risk merchants that have been declined or restricted by conventional providers - and shares his experience and best practices on this blog.

Tailored payment solutions for high-risk merchants

- Domestic and offshore accounts

- Competitive, interchange plus pricing

- No long-term contracts or hidden fees

- Built in fraud protection

- Dedicated account manager; 24/7

Sign up in 5 minutes

A+ Rating

as of 06/17/26

Related Posts

![Shopify High-Risk Payment Processors in 2026 [Reviewed & Ranked]](https://secureglobalpay.net/wp-content/uploads/Shopify-1-300x158.jpg "Shopify High-Risk Payment Processors in 2026 [Reviewed & Ranked]")